Schedule Appointment »

702-660-7000

702-660-7000

Typical Financial Planning:

The type of financial planning in use today encourages you to put your money where there is a risk you could lose the money. The truth is, the only place you can keep your money safe from loss is in certain Bank products and in specific Life Insurance contracts which legally guarantee that you won’t lose your money.

Yet, it’s true that Bank products and Insurance contracts don’t provide high rates of return on your money because the banks and the insurance companies are assuming 100% of the risk for you. That is why typical financial planners try to persuade you to assume more risk, so your money has a higher chance of earning a higher rate of return.

The problem is, this added risk may not be something that you can afford to assume. Regardless of that fact, the financial planner recommending you to assume the greater risk will be paid regardless if the higher return is achieved for you or not.

Risk Tolerance:

The typical financial planner will determine what your risk tolerance is based on your age, your income, and the growth you would like to achieve. The younger you are, the higher your risk tolerance will be. But even if you are retired you may be placed in a higher risk tolerance bracket than what you are comfortable with due to the growth portion of this 3-part equation.

The typical financial planner will determine what your risk tolerance is based on your age, your income, and the growth you would like to achieve. The younger you are, the higher your risk tolerance will be. But even if you are retired you may be placed in a higher risk tolerance bracket than what you are comfortable with due to the growth portion of this 3-part equation.

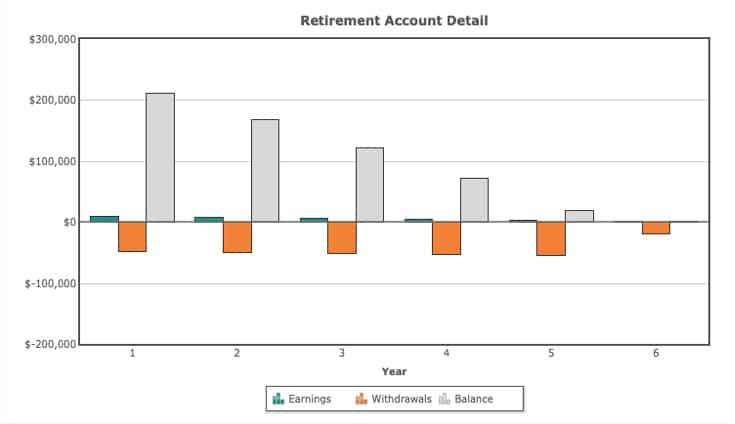

For example, if you are 65, but only have $250,000 saved for retirement, you will need to have a lot of growth in order not to run out of money before you die. That is because $250,000 earning a 4% rate of return, will only last 5.5 years, if you need $65,000/year to live on in retirement. That is why you could end up in a higher risk tolerance bracket when you should be in a position of avoiding risk.

Another way you may be placed into a higher risk tolerance bracket is if you are young. According to typical financial planning, you can afford to take higher risks when you are younger. But assuming higher risk means you also assume a higher probability of losing the money you have saved, and that violates Warren Buffett’s first rule of creating wealth, “Never Lose Money.” [1] Losing money forces you to start over again, or at least recover your losses. Yet starting over again later in life means you will have to assume even higher risks in attempts to make back what you have lost.

Here is the rub. What typical financial planners classify as a recovery doesn’t take into consideration the time lost during the recovery period. That time is lost to you forever. Meaning, if you lose part of your savings several years into your retirement plan, as many did in 2008 and many are doing so today, you will have to save much more money out of your income to come even close to what you had planned on saving for your retirement, even if your investment recovers the loss that you experienced.

This isn’t just this author’s crazy impression.

Obviously, moving to cash and cash equivalents is a valid point for many who cannot and should not be assuming higher risks in hopes of experiencing more growth. Growth is not guaranteed simply because you assume higher risks and that is why traditional, rather than typical, financial planning always focuses on protection first!

Holding cash and cash equivalents such as certain types of Bank products and Life Insurance Contracts that guarantee values, is smart money management. These products and contracts safeguard what you have saved and still provide moderate growth over time, which is the very things you cannot afford to lose. A steady moderate guaranteed tax-free growth rate of 5% will outperform a riskier nominal rate of return of 7%, even when the projected 7% benchmark rate of return is hit. This is due to taxes, management fees, marketing expenses, and trading fees which can easily knock off 2% or more of the growth on an investment making the 5% guaranteed growth fund more profitable for you without assuming higher risk.

Of course, with the higher risk there is always the risk of losing more than the growth you experience. You could actually lose your invested capital making the risk intolerable.

Loss Avoidance Factor:

Traditionally, it was considered germane to protect what you saved in order to avoid losses. A good way to discover your risk tolerance is to consider what your loss avoidance is. For example, would you risk $1,000 to earn

Most investors will not risk $1,000 to earn less than $1,000. $1,000 would be their loss avoidance factor. Historical data can assist you in finding your loss avoidance factor but can never provide you with the legally binding contract which will guarantee that you will never earn less, or lose more. Only certain Banking products and specific Whole Life Insurance Contracts can provide you that guarantee.

Why Whole Life Insurance?

Whole life insurance contracts are not based on you earning a rate of return but rather on you owing a larger and larger portion of your death benefit as time progresses. Equity developed overtime like this can be guaranteed to the policy holder due to the actuarial science which provides the basis of all insurance coverage. The insurance company knows beforehand what the risks are and assumes those risks for you, while providing you with the coverage you need and the opportunity to own the asset you are purchasing…the death benefit.

The death benefit, which you own, has a value which the insurance company calls cash value. It is this cash value that you can leverage and use while still living without reducing the continual growth of your ownership in the policy. Thus, your whole life insurance policy will continue to experience growth regardless of whether you leverage it or not. All you are required to do is to pay the agreed upon premium and any interest owned on any money you’ve borrowed against your policy’s cash value.

At the same time policy holders can also earn dividends. Dividends, like with any company, are decided upon by the board of directors at the end of a fiscal year. Once determined, they are paid to the policy holders, and don’t merely dilute your stock holdings as they would when paid to common stock holders of a publicly traded company.

The policy holder can choose to have the dividends purchase more insurance coverage in the policy which will increase the ownership of the policy holder. In doing so, the policy holder will be eligible for a larger share of the dividend the next time the board of directors declares a dividend.

The Importance of Dividends:

Dividends are the key to long-term growth![3] Dividends are paid by companies that are solid and reliable. Dividends have been a substantial measure of a company’s ability to earn profits and for the first 45 years of the S&P 500 the average dividend never fell below 3%.[4] But due to the Federal Reserve, cheap money forced prices up and dividends down.[5] Even so, Standard and Poor’s estimates that more than $7.8 trillion is benchmarked to the S&P 500 and since March of 2010 and March 2020, 2.11% of total gains have been due to dividends.[6]

Interestingly, mutual life insurance companies have a tremendous record of paying dividends consecutively year after year for well over 100 years. This is a strong record that only 15 publicly traded companies have been able to manage.[7] Dividends then are another reason traditional financial planning was based on owning participating whole life insurance. With such an amazing dividend track record it was, and still is, a solid foundation to build wealth.

Conclusion:

There is a time and place for taking risk(s). But not when you are young and not when you are old. In fact, time shouldn’t be a factor in determining your risk tolerance. You should only take risk(s) when you can afford to lose the money invested and not be hurt financially, i.e., not have to lower your standard of living if you lose the money invested.

Following this one rule you will be able to enjoy the benefits of compounding growth, which has been called the 8th wonder of the world. Compounding growth really only becomes advantageous once it becomes exponential. And exponential growth takes time without loss or interruption. Time without loss or interruption is guaranteed in participating whole life insurance contracts. But if your time here on earth is interrupted or lost, your beneficiary(s) will have more money than you could have saved for them. And it will be income tax free!

Dr. Tomas P. McFie

Dr. Tomas P. McFie

Most Americans depend on Social Security for retirement income. Even when people think they’re saving money, taxes, fees, investment losses and market volatility take most of their money away. Tom McFie is the founder of McFie Insurance which helps people keep more of the money they make, so they can have financial peace of mind. His latest book, A Biblical Guide to Personal Finance, can be purchased here.

[1] https://www.investopedia.com/financial-edge/0210/rules-that-warren-buffett-lives-by.aspx

[2] https://www.theatlantic.com/business/archive/2015/10/the-recession-hurt-americans-retirement-accounts-more-than-everyone-thought/410791/https://www.theatlantic.com/business/archive/2015/10/the-recession-hurt-americans-retirement-accounts-more-than-everyone-thought/410791/

[3] https://finance.yahoo.com/news/10-rules-made-warren-buffett-230758470.html

[4] https://www.investopedia.com/articles/markets/071616/history-sp-500-dividend-yield.asp

[5] https://www.investopedia.com/articles/markets/071616/history-sp-500-dividend-yield.asp

[6] https://dqydj.com/sp-500-return-calculator/

[7] https://www.dividend.com/how-to-invest/15-companies-that-have-paid-dividends-for-more-than-100-years/