Schedule Appointment »

702-660-7000

702-660-7000

Understanding life insurance is a wise investment of your time. It’s not just a safety net for your loved ones in the event of your passing, offering a death benefit, but it’s also a financial tool you can benefit from during your lifetime. A well-chosen life insurance policy allows you to securely grow your funds and provides the flexibility to access these funds for opportunities that might otherwise be out of reach with different financial strategies.

All life insurance policies offer a death benefit to your beneficiaries if you pass away while the policy is active, a fact widely recognized.

However, what’s less known is the living benefits of life insurance. When utilized effectively, life insurance can serve as a financial asset during your life. This life insurance 101 guide will shed light on the benefits of life insurance and help you determine which policy suits your needs. We’ll start with an overview of the various types of life insurance.

“There are two basic kinds of life insurance policies: Paid-up permanent, and term insurance.”

Whole life insurance, the most traditional form of permanent insurance, is designed to last your entire lifetime. Beyond offering the standard death benefit, these policies can also provide a feature known as “living benefits,” accessible while you’re still alive. This is achieved through building cash value within the policy, either through direct premium payments or, in the case of participating whole life policies, through dividends from the insurer’s surplus profits.

The cash value in whole life policies grows on a tax-deferred basis, and as the policyholder, you can borrow against this cash accumulation without facing immediate tax consequences. Alternatively, you can opt to surrender part of the insurance to withdraw from the cash value.

It’s crucial to understand the potential tax implications and how such actions might affect the policy’s death benefit, future dividends, and applicable interest charges. Whole life insurance not only meets basic insurance needs but also serves as a tool for wealth growth and seizing financial opportunities throughout your life.

| Tools of the Trade - How to Use the Cash Value in Your Life Insurance A quick reference guide on how policy loans work, how to make loan repayments and how to track your loans. |

Also see: What Is Participating Whole Life Insurance?

Term Life Insurance is a another form of life insurance, this time designed for temporary coverage.

This type of insurance is set up to last for a certain period, like 10 to 30 years, not your entire life. Some term life policies offer fixed premiums for the duration of the policy, meaning you’ll pay the same amount each year. Others might have premiums that renew annually, which typically increase as you age. It’s crucial to stay up-to-date with your term insurance to ensure that your loved ones are protected with the death benefit if something happens to you.

Understanding the Infinite Banking Concept and How It Works In Our Modern Environment 31-page eBook from McFie Insurance Order here>

In addition to the basic types of life insurance, there are also more complex options available in the market that blend elements of the traditional policies with investment components.

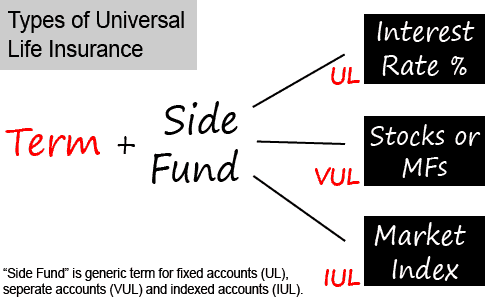

Universal Life Insurance (UL) combines aspects of term life insurance with a savings element that is somewhat similar to a money market investment. This type of insurance offers flexibility and the potential for cash value growth, with the investment returns being subject to change monthly.

Variable Life (VL) Insurance is a form of permanent life insurance that is often seen as the priciest option for cash-value insurance. In this policy, the cash value and the amount you pay in premiums are tied to the performance of investments that you choose. While the potential for higher returns is there, so is the risk, along with typically higher fees. Despite the investment risks, most VL policies guarantee a minimum death benefit.

Variable Universal Life (VUL) Insurance is another permanent life insurance option where the cash value is invested in what are known as separate accounts, which function similarly to mutual funds. This offers a way to potentially increase the cash value of your policy through investments, though it comes with its own set of risks and rewards.

Indexed Universal Life (IUL) Insurance is a newer form of permanent life insurance that combines a guaranteed interest rate with the potential for additional interest tied to the performance of a market index, like the S&P 500. In IUL policies, your premiums go into a fixed account that earns interest. The interest rate varies, offering both a minimum and a maximum cap. You have the option to allocate a portion of your funds from the fixed account to an indexed account, where the interest earned matches the index’s performance.

When considering VL, VUL, and IUL policies, be aware they come with various fees and costs beyond just the insurance charges, including surrender fees and other expenses. These can significantly affect the value of your policy and its tax implications. That’s why it’s essential to consult with a financial advisor or insurance agent, as well as a tax professional, before making any decisions about your life insurance.

As financial advisors, we’re here to guide you through choosing the right type of life insurance, designing a policy that suits your needs, and using it effectively to grow your wealth quickly. Understanding the nuances of life insurance is crucial for making informed decisions that align with your long-term goals.

To learn more about life insurance, read the next installments in the Understanding Life Insurance series.

Get a working knowledge of how each type of life insurance policy works.

After reading this 10-page booklet you'll know more about life insurance than most insurance agents.

Download here>

Note: Loans and withdrawals from life insurance can cause adverse tax consequences, penalties and may cause a policy to lapse. Insurance products are backed by the claims paying ability of the issuing insurance company and are not FDIC insured. McFie Insurance, its agents, and representatives are not authorized to give legal or tax advice. Read Full Disclaimer

by John T. McFie

by John T. McFie

I am a licensed life insurance agent, and co-host of the Wealth Talks podcast.

At age 14 I started developing spreadsheet models and software systems to help my Dad share financial concepts with clients.

Skipped college at 17 recognizing the overinflated value and prices of most college degrees and built more financial software instead (see MoneyTools.net). Still a strong advocate of higher education without going to college. I enjoy making financial strategies clear and working through the numbers to prove results you can count upon.