Schedule Appointment »

702-660-7000

702-660-7000

QUICK TIP: You can use your keyboard command (Ctrl + F) on your Windows or (Cmd + F) on a Mac to search this page.

Your Financial GAME™ (YFG): A trademarked phrase of McFie Insurance, Inc. and Your Wealth Team

G = Guaranteed

A = Available

M = Manageable

E = Equity

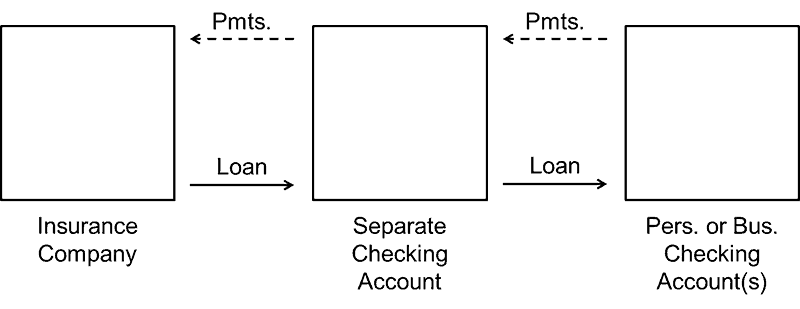

separate checking account/money manager account: A personal checking account we recommend you setup to help simplify and track the flow of money in your personal finance system; Loans from multiple life insurance policies will go into your separate checking account, and loans to yourself, your business and/or other sources will come out of it. Repayments on loans made from this account come back to the account.

Example:

Note: Do not confuse this term with separate accounts at the insurance company that are used to segregate funds from variable life insurance products for investing purposes. The separate checking account we are referring to with this term has nothing to do with the insurance company or investments. It is a normal personal checking account at a commercial bank.

| Tools of the Trade - How to Use the Cash Value in Your Life Insurance A quick reference guide on how policy loans work, how to make loan repayments and how to track your loans. |

Infinite Banking Concept, Becoming Your Own Banker, Bank on Yourself, Bank of You, Banker’s Table, BOSS Wealth System: Trademarks and copyrighted terms used to describe the process of using whole life insurance as a savings vehicle and taking a policy loan to finance investments and/or purchases; Many life Insurance agents/producers profess to teach these concepts and some do a better job than others. The underlying idea of using whole life insurance as a savings vehicle is very good because 1) you can get a guaranteed return, 2) death benefit protection, and 3) still have access to money via policy loan from the insurance company.

Note: Some insurance agents try to use universal, variable, variable universal or even equity-indexed universal life insurance policies in teaching these concepts which do not work the same way as whole life insurance and subject the policy owner to risk.

actual rate of return: The yield, or return on an investment as opposed to an estimation or average of the same

annual percentage rate: The interest rate for a whole year (annualized), rather than just a monthly rate

annual rate of return: The ratio of money gained or lost (whether realized or unrealized) on an investment; also known as return on investment, rate of profit or sometimes just return

average rate of return: Determined by taking the total cash inflow/outflow over the life of the investment and dividing it by the number of years in the life of the investment; not a guarantee that the cash flow will be the same in every given year of the investment

bank: A financial institution that accepts deposits and channels the money into lending activities

banker: A financier who owns or is an executive in a bank

banking/banking equation: The flow of money from one entity to another facilitated by an intermediate who earns a profit from the transaction

borrow: To receive something with intent to repay

capital: The factor of production used to create goods or services that is not itself significantly consumed, though it may depreciate in the production process

compound interest: Interest that accrues on the initial principal as well as the accumulated interest of the principal, loan or debt; allows a principal amount to grow at a faster rate than simple interest, which is calculated only on the principal amount

Example: If you start with $100 earning 5% annually, then at the end of one year you will have $105. Repeat the process using the $105 as your capital and after the second year you will have $110.25.

Economic Value Added (EVA): A registered trademark of Stern Stewart & Co.; an estimate of a firm’s economic profit – being the value created in excess of the required return of the company’s investors; The concept recognizes the crucial fact that there is a cost to capital even if that capital is your own capital. This paradigm shift is important in understanding the full potential of Your Financial G.A.M.E.TM

equity: The value of an ownership interest in an asset

inflation: An erosion in the purchasing power of money – a loss of real value in the internal medium of exchange and unit of account in the economy

interest: A fee paid on borrowed assets; the price paid for the use of borrowed money; money earned on deposited funds

investment: The commitment of money or capital to the purchase of financial instruments or other assets in the hope of earning a profitable return

life insurance: Protection against loss of income if the insured passes

leverage: The use of various financial instruments or borrowed capital, such as margin, to increase the potential return of an investment; the amount of debt used to finance a firm’s assets; A firm with significantly more debt than equity is considered to be highly leveraged.

money: A medium of exchange; usually an officially-issued legal tender defined by government

payment: The exchange of wealth from one party to another

principal: The amount borrowed; the portion of a payment which is not interest; With a loan amortization schedule, the principal and interest are separated, indicating which part of the payment goes to paying off the principal, and which part is used to pay interest.

rate of return: Used to describe the rate that an investment grows during a given period; very similar to the annual percentage rate on a loan only the money is received instead of paid

Example: If you give your friend a loan at 10% annual percentage rate, then you make a 10% annual rate of return.

Rate of Return is also similar to the annual percentage rate on a loan because, by itself, it doesn’t tell you the whole story.

Example: Suppose you found an investment that could promise you a 25% guaranteed annual rate of return over 2 years. You invest $10K locking it away for 2 years. You earn 100% the first year doubling your initial investment, but then next year you lose 50% of $20k down to $10K so now you’re back right where you started, but that’s a 25% guaranteed annual rate of return. (100% – 50%) / 2 years = 25%

reserves: A stockpile

risk: Uncertainty regarding the possibility of loss

savings: Income not spent, or deferred consumption

shareholder: One who owns shares in a company; a stockholder; a partner

stock: A security which signifies ownership in a corporation and provides a claim on a portion of that corporation’s assets and earnings; A common stock allows for the owner to vote, attend shareholder’s meetings and receive dividends. A preferred stock typically doesn’t allow voting privileges but has a higher claim on assets and earnings.

time value of money: The compounding process of money

Velocity of Money: The process of quickly taking incoming payments and loaning them back out again so the money is earning the maximum interest possible

Volume of Interest: Defined as the Total Interest/Total Payments over a specified period of time; not to be confused with the annual percentage rate (APR)

Example:

A loan for $20,000 at 7% APR for 48 months results in a monthly payment of $478.92

Volume of Interest = Total Interest/Total Payments

Total Payments = 478.92 x 48 = 22,988.16

Total Interest = Total Payments – Principal = 22,988.16 – 20,000.00 =2,988.16

Volume of Interest = 2,988.16/22,988.16 = 0.1299 (about 13%)

wealth: The abundance of valuable resources or possessions (material or spiritual) or the control of such assets

yield: The amount of profit that returns to the owner

Equity Indexed Universal Life Insurance (EIUL): A sort of middle ground between Universal Life and Variable Universal Life Insurance; The cash fund of Equity Indexed Universal Life Insurance is neither tied to an interest rate nor invested directly in stocks, but is rather tied to an index of stocks hence the name “equity indexed.”

Participating Whole Life Insurance (WL or PWL): Designed to remain in force for the insured’s “whole life.” “Participating” simply means that the insurance company shares excess profits (variously called dividends or refunds in the United States) with the policy owners. The basic design of Whole Life Insurance requires premiums to be made every year, but there are ways to design the policy to become “paid-up” at an earlier time. Whole Life Insurance has been around for 200 years in the United States and is very stable. The insurance company takes all the risk and provides a guarantee of policy values regardless of market conditions, as long as the policy owner meets premium requirements and pays interest on any outstanding loan. The unique design makes this type of insurance policy a very good vehicle for long-term, predictable financial results.

Single Premium Insurance: A type of life insurance where one premium is paid to purchase insurance that covers the insured for life; The greater part of the premium on an insurance policy like this goes right to cash value, however the policy owner is discouraged from taking a policy loan or otherwise accessing the cash value because of the tax code which classifies this type of policy as a modified endowment contract according to the 7-pay test.

Term Insurance: The original form of life insurance; provides coverage for a limited period of time; Term insurance can be purchased as a stand-alone insurance product or added on as a rider to a permanent policy. Most term insurance is designed to take level premiums and provide a fixed amount of coverage over a period of 10-30 years. One-year term insurance requires yearly increasing premiums to maintain a fixed amount of coverage.

Universal Life Insurance (UL): Essentially one-year term insurance combined with a cash fund that earns a rate of interest; As the insured gets older and the cost of the insurance part of the policy increases, the cash fund is designed to offset the extra premiums required, but it does not always do so, especially when interest rates are low. Many universal life insurance policy owners have to put more money into the policy in later years to keep it alive.

Variable Life Insurance (VL): Generally the most expensive type of cash value life insurance because it allows the policy owner to allocate a portion of the premium dollars to a separate account comprised of various instruments and investment funds within the insurance company’s portfolio such as stocks, bonds, equity funds, money market funds etc.; In addition, because of investment risks, variable policies are considered securities contracts and are regulated under the federal securities laws; therefore, they must be sold with a prospectus. The major advantage to variable policies is that they allow the policy owners to participate in various types of investment options while not being taxed on the earnings (until the policy is surrendered). Policy owners can also apply the interest earned on these investments toward the premiums, potentially lowering the out-of-pocket outlay. However, due to investment risks, when the invested funds perform poorly, less money is available to pay the premiums, meaning that the policy owner may have to pay more than they can afford to keep the policy in force. Poor fund performance also means that the cash and/or death benefit may decline, though never below a defined level.

Variable Universal Life Insurance (VUL): Very similar to Universal Life Insurance, except that instead of the cash fund earning an interest rate, it is allocated into separate accounts for investment in stocks (similar to Variable Life Insurance); The policy owner gets to choose the separate accounts among which to allocate the cash fund. Depending on market performance more premium may be required to keep up the insurance part of the product, and thus the policy owner takes on extra risk.

7-pay test: A tax code limitation designed to discourage life insurance premium schedules that would result in a paid-up policy before the end of a seven-year period. A policy that does not meet the 7-pay test is classified as a modified endowment contract.

cash fund: The accumulated money that earns a rate of interest in Universal Life Insurance Policies

cash value: The money offered to the policy owner by the issuing life insurance carrier upon cancellation of the contract; depending on contract terms, cash value can often be used as collateral for a loan from the insurance company; also called the cash surrender value or surrender value

death benefit: The money payable to beneficiary(s) upon the death of the insured; can be different than the face value (see face value) stated in the policy depending on special riders and/or an outstanding policy loan

direct versus non-direct recognition: Two different methods insurance companies use to calculate dividends on whole life insurance policies with an outstanding loan; With a non-direct recognition contract, the dividend earnings rate is totally unaffected by any policy loans. With a direct recognition contract, the dividend earnings rate can be affected positively or negatively when cash value is used as collateral for a loan.

Generally, with a direct recognition contract, the collateralized cash value has a dividend rate that is a certain number of basis points lower than the interest charged on the loan. If the current-gross-dividend-crediting rate is less than the gross-direct-recognition-crediting rate, then the collateralized cash value is affected positively. If the current-gross-dividend-crediting rate is greater than the direct-recognition-crediting rate, then collateralized cash value is affected negatively.[i]

dividends: A distribution of a portion of a company’s earnings, decided upon by the board of directors; With mutual life insurance companies this distribution is technically a “return of premium” thus life insurance dividends are not currently taxable income to a policy owner.

Note: Dividends can be taxed upon withdrawal when the overall withdrawals exceed the cost basis of the policy.

face value/face amount: The amount of insurance purchased and stated in the policy; actual death benefit (see death benefit) can be different depending on special riders and/or an outstanding policy loan

modified endowment contract: A life insurance policy that becomes a modified endowment contract, according to the 7-pay test, discourages cash value access by the policy owner because policy loans and withdrawals face taxes and penalties very similar to monies from a qualified plan.

mutual vs. stock-held insurance company: A mutual company is owned by its policy holders. A stock-held company is owned by outside stockholders.

premium: A payment for insurance

rider: A feature added to a basic insurance policy; There are many different kinds of insurance riders. Some of these are explained below.

Accidental Death Benefit Rider (ADBR): Increases the death benefit (typically by 2 or 3 times) of a life insurance policy in the event that the insured dies in an accident

Enhanced Blended Insurance Rider (EBIR): Blends one-year term insurance and paid-up insurance resulting in a specified coverage amount

Living Benefits Rider or Accelerated Benefit Rider: Allows a policyholder access to a portion of the death benefit of their policy in the case they become terminally ill and a doctor has given them an estimated time left to live

Paid-Up-Additions Rider (PUAR): Adds single premium insurance to a basic whole life insurance policy; Using this rider does not have to make the policy a modified endowment contract as long as the combined policy meets the 7-pay test.

Waiver of Premium Disability Rider (WPD): Covers premiums on the life insurance policy if the insured becomes disabled according to the terms listed in the contract

[i] Todd Langford, How to tell the whole truth about Direct Recognition, truthconcepts.com, September 26, 2011