Email Us Now

Email Us Now 702.660.7000

702.660.7000Schedule Appointment »

702-660-7000

702-660-7000

Becoming debt-free can be an incredibly daunting task, one that many people might never experience. Debt is a common aspect of modern life, whether it’s taken on voluntarily or involuntarily. Voluntary debt includes things like student loans and credit card debt, while involuntary debt arises from emergencies. Regardless of how it comes about, to truly be debt-free, you must eliminate all debts—none, zero, zilch.

This brings to mind a beloved story from the “Frog and Toad” series called “Cookies.” In the story, Toad bakes delicious cookies and shares them with Frog. They both enjoy the cookies so much that they can’t stop eating them, even while discussing how they need to stop. They try various methods to resist—putting the cookies in a box, tying the box with string, and placing it on a high shelf—but each time, they find a way to get back to the cookies.

Finally, they decide to throw the cookies out to the birds, symbolizing the need for willpower. Frog then says, “Now we have lots and lots of willpower,” to which Toad replies, “You can keep all the willpower. I’m going home to bake a cake.”

This story illustrates the struggle many people face when trying to get out of debt. They go through various steps to make it harder to access their credit, such as freezing their credit cards in ice. However, these measures only make it more difficult rather than addressing the core issue of debt itself.

Rather than attempting to become debt free, which is practically impossible, we encourage people to become free of debt. This simple shift in wording helps us see that not all debt is bad when it is managed properly.

The first step to becoming free of debt is to sit down and assess your financial situation. This process requires a thorough understanding of where your money is going. Think of it like finding your location on a map in a new mall before heading to your destination.

Without a clear picture of your starting point, it’s impossible to navigate a path to debt freedom.

Begin by gathering all your financial documents, including bank statements, credit card bills, loan statements, and any other relevant financial information. Make a list of all your debts, including the creditor, the total amount owed, the interest rate, and the minimum monthly payment. Next, list all your sources of income. This comprehensive overview will help you understand your financial position and identify areas that need improvement.

Creating a realistic budget is crucial in your journey to becoming debt-free. A budget is a financial plan that includes all your income and expenses. Start by categorizing your expenses into fixed (e.g., rent or mortgage, utilities, insurance) and variable (e.g., groceries, entertainment, dining out). This categorization will help you see where you can cut costs.

Remember, being free of debt doesn’t mean you won’t have any bills. Essential expenses like utilities, property taxes, and insurance are part of life and must be accounted for in your budget. A realistic budget helps you manage these ongoing expenses while working towards eliminating your debt.

Use budgeting tools or apps to track your spending and adjust your budget as needed to ensure you stay on track.

|

Financial Decision Making 16-page Slide Deck If you do some of the right things financially, but do them in the wrong order, your finances will suffer. This quick guide gives you 4 easy steps in order of priority. |

Changing your mindset about spending is a critical component of becoming free of debt. Just as Frog and Toad had to control their cookie-eating habits, people in debt need to develop better spending habits. This means recognizing and modifying behaviors that lead to unnecessary spending.

Start by distinguishing between wants and needs. Needs are essential for survival, such as food, housing, and healthcare, while wants are non-essential items that you can live without. By focusing on needs and limiting wants, you can redirect funds towards paying off your debt. This mindset shift requires discipline and commitment but is essential for long-term financial health.

To accelerate your journey to becoming free of debt, identify areas where you can cut back on expenses. This might mean reducing the frequency of dining out, canceling unused subscriptions, or finding cheaper alternatives for everyday items. However, cutting expenses doesn’t mean you have to eliminate all pleasures from your life.

Plan when and how you will indulge in luxuries responsibly. For instance, if you love getting coffee, you don’t have to give that up entirely. Instead, make it a treat rather than a daily habit. By making mindful decisions about spending, you can still enjoy the things you love without derailing your financial goals.

Sometimes, cutting expenses alone isn’t enough to pay off your debt quickly. Increasing your income can significantly accelerate your progress. Consider taking on a second job, freelancing, or starting a side hustle. These additional income streams can provide extra funds to pay down your debt faster.

Additionally, look for opportunities to increase your income at your current job. This could involve asking for a raise, working overtime, or seeking a promotion. Addressing the root of your financial issues often requires a combination of reducing expenses and boosting income.

The 10-20-70 principle is a simple yet effective budgeting guideline to help manage your finances. According to this principle, you should allocate:

Adhering to the 10-20-70 principle helps create a balanced approach to managing your finances. It ensures you are saving for the future, aggressively paying down debt, and covering your necessary living expenses without overspending.

By following these steps and principles, you can develop a clear, actionable plan to become free of debt. Remember, the journey to financial freedom requires patience, discipline, and a commitment to changing your financial habits. But with a well-thought-out plan and the right mindset, you can achieve and maintain a lifestyle free of debt.

Living free of debt is different from just being free of debt. Being free of debt might mean you have no debts at a given moment, but living free of debt means you have a sustainable plan to manage and avoid unwanted debt. It involves building a lifestyle that prevents debt accumulation and ensures financial stability.

The journey to becoming and living free of debt requires a combination of self-discipline, strategic planning, and sometimes, a change in lifestyle or mindset. It’s about making conscious choices that align with your long-term financial goals and understanding that the freedom from debt comes with the responsibility of maintaining good financial habits.

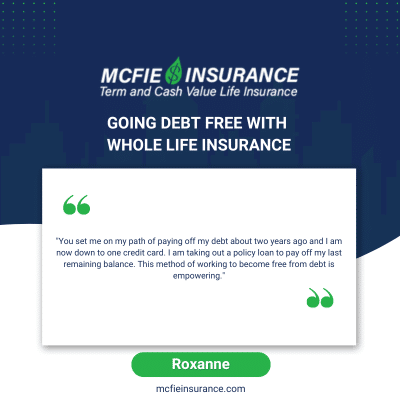

Whole life insurance, a type of permanent life insurance, can be a powerful tool in your journey to becoming free of debt. Unlike term life insurance, which only provides coverage for a specific period, whole life insurance offers lifelong coverage and includes a cash value that grows over time. This cash value can be leveraged in various ways to help you manage debt and improve your financial stability.

Whole life insurance policies consist of two main parts: the death benefit and the cash value.

One of the key benefits of whole life insurance is the ability to borrow against the cash value. Here’s how you can use it to become free of debt:

Assess Your Policy: Review your whole life insurance policy to understand the cash value and the terms of borrowing against it.

Calculate Your Debt: List all your debts, including interest rates and balances. Identify which debts are high-interest and should be prioritized for repayment.

Borrow Strategically: Consider taking a policy loan to pay off high-interest debt. Use the loan to consolidate multiple debts into a single, lower-interest loan.

Repay the Loan: Develop a repayment plan for the policy loan. While there is flexibility, repaying the loan will restore the full death benefit and prevent the loan from accruing interest.

Monitor Your Policy: Keep track of your policy’s cash value and any outstanding loans. Ensure that your policy remains in good standing and continues to grow.

|

Policy Checklist Make Sure You Get a Good Policy Is your policy good or bad? Use this checklist to help evaluate your existing life insurance or a new policy you are considering. |

Whole life insurance can be a valuable tool in your strategy to become free of debt. By leveraging the cash value of your policy, you can access funds at lower interest rates, repay high-interest debt, and improve your financial stability.

It’s crucial to use this strategy wisely and maintain your policy to ensure it continues to provide financial protection for you and your loved ones.

Schedule a consultation with McFie Insurance today and start your journey to living free of debt.