Email Us Now

Email Us Now 702.660.7000

702.660.7000Schedule Appointment »

702-660-7000

702-660-7000

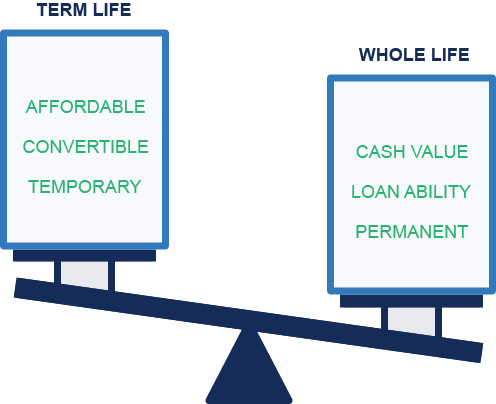

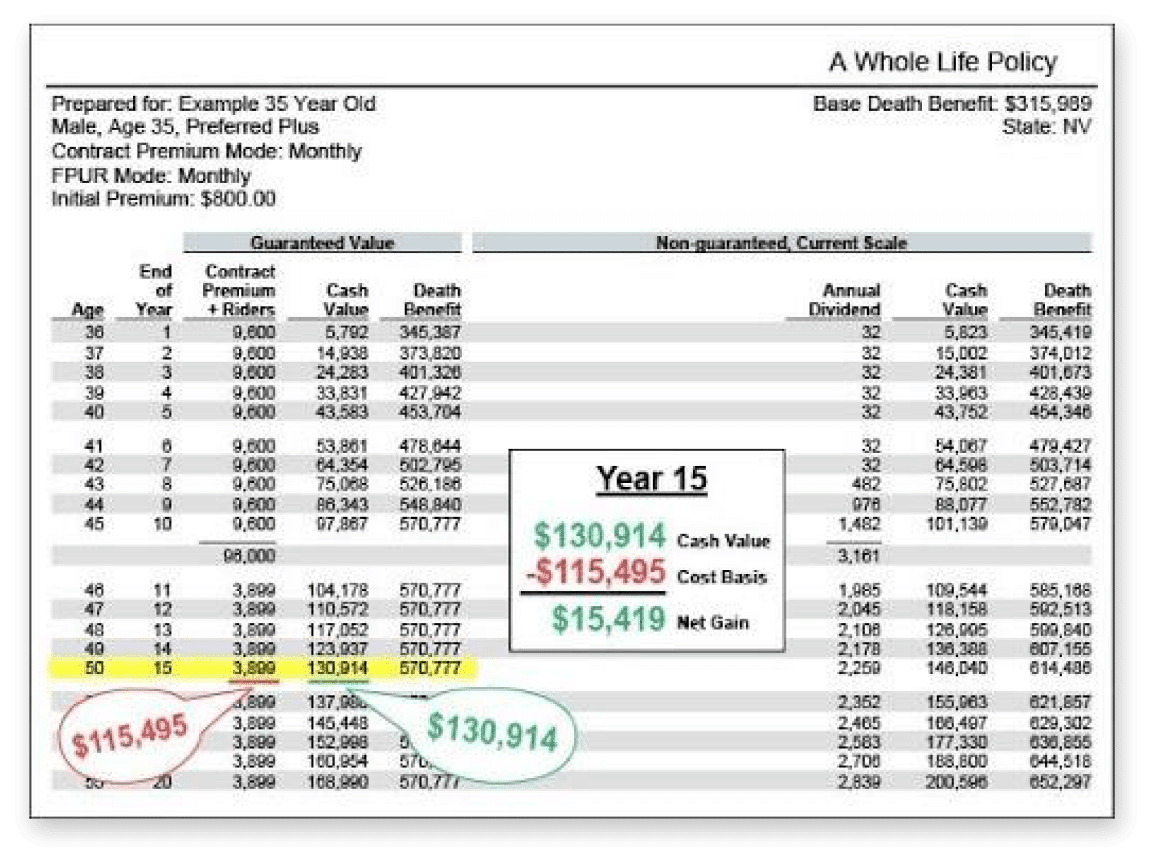

Whole life insurance is the best type of policy for a guaranteed death benefit, guaranteed cash value, and for building your wealth throughout your entire life, not just a specific time period.

Term life insurance only protects you for a certain number of years while whole life protects you for your entire lifetime..

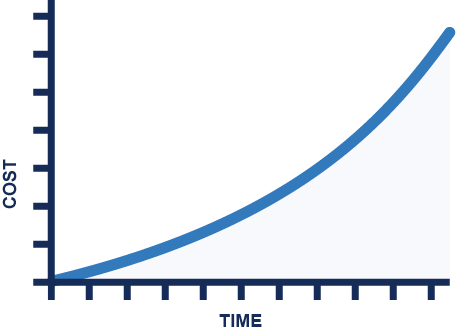

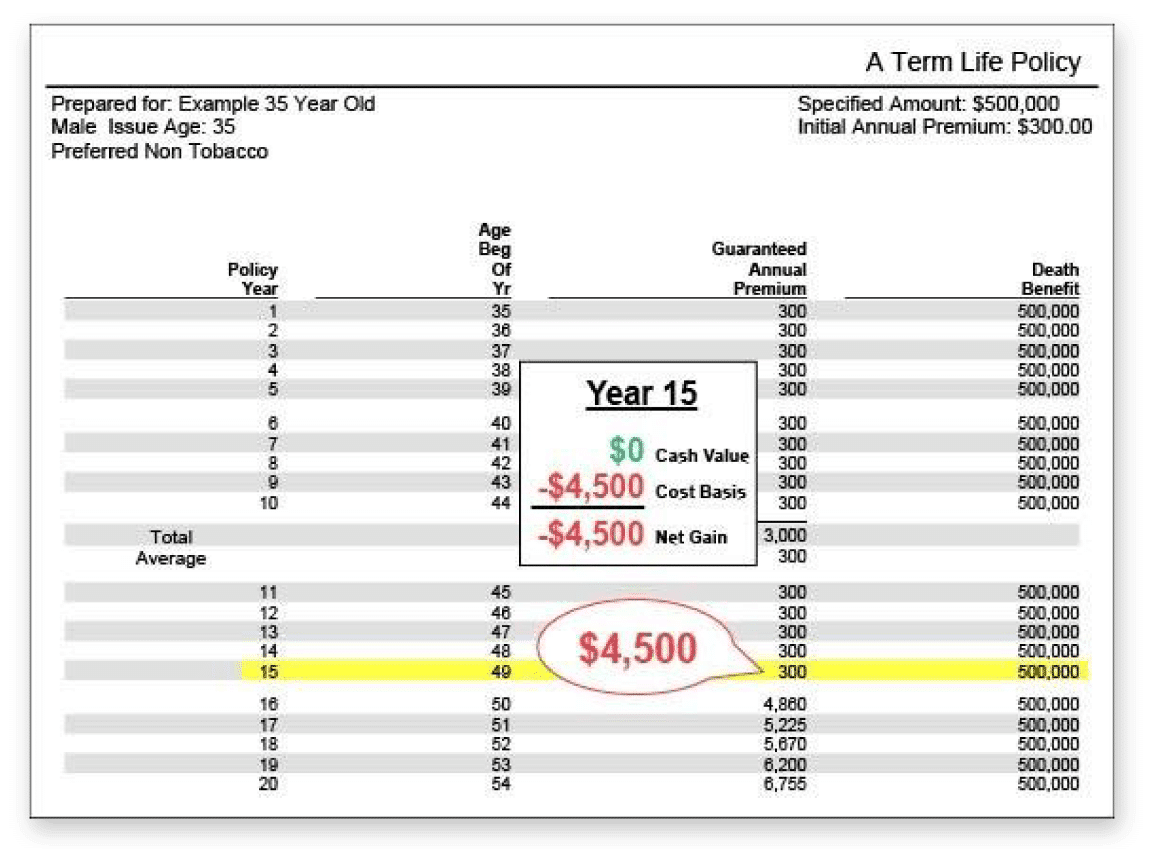

Term life premiums may initially be less expensive than whole life, but its premiums continue to increase in cost over time if you keep the policy beyond the level term period, and you won’t build any cash value.

this death benefit is only paid out if you die during the term of your coverage. This is the caveat to term insurance.

whole life insurance is a permanent type of insurance that provides a death benefit for your entire life with guaranteed tax-free growth and easily accessible cash value.

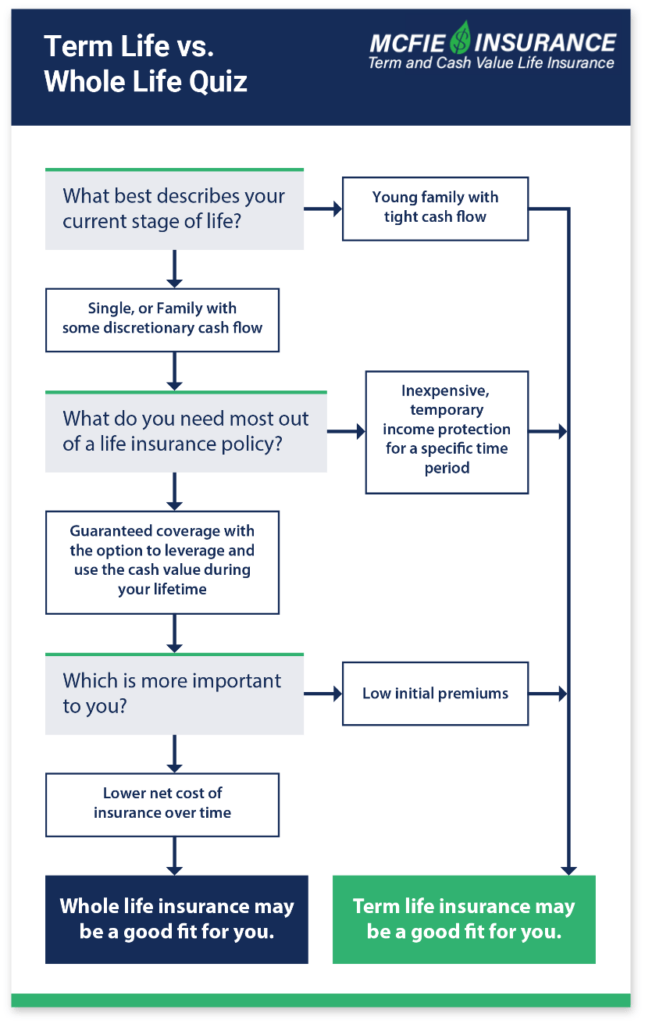

There are a lot of things to consider and opinions to sift through when choosing between term vs. whole life insurance. Here are a few standard questions you can answer to help better determine what coverage would be best for you outlined in the quiz below.