Schedule Appointment »

702-660-7000

702-660-7000

According to the Federal Reserve Bank, Americans who are 55-59 have saved $223,493 towards their retirement. Those 60-64 have only saved $221,451 and those who are 65-69 have saved even less, $206,819.

Obviously, these balances are averages, but it is important to appreciate that Fidelity, who manages about 2/3 of America’s retirement savings plans reports there is only 1.6% of those plans which contain more than $1 million.

Is $1 million dollars enough to sustain you throughout your retirement? And even if it is, what guarantees do you have that you will become one of the 1.6%, who actually becomes a 401(k) or IRA millionaire before retirement?

These are not silly questions. They are questions that you should be asking yourself now rather than later. Furthermore, knowing the average retirement savings account is basically 75% underfunded if $1million is the desired goal, everyone should be exploring the options to build sustainability for their retirement years and the sooner the better.

Back in 1933 George Clason detailed the 10-20-70 principle in his legendary book entitled, The Richest Man in Babylon. By living on 70% of your income and using 20% of your income to pay revolving debt like credit cards or personal lines of credit, you can keep 10% of your income.

If you use your 10% to purchase participating whole life insurance over your lifetime, while earning at least what the average wage earner earns in the United States, you will have over $580,000 of guaranteed cash value available in your life insurance policies for your retirement by age 67.

$580,000 is 64.34% more than what the average American has saved up by age 67!

$580,000 is 64.34% more than what the average American has saved up by age 67!

And all of that $580,000 will be available to you to use without having to pay taxes, like you would on a 401(k) or IRA saving account.

Waiting for a better time to start keeping your 10% will end up costing you dearly. For example:

In fact, starting 15 years early will cost you 120% less in contributions than starting 15 years later. You will also end up with 39.88% more in your account balance at the end of 47 years than if you start 15 years later, even though you will have paid 120% less for this extra growth. Finally, you will have the advantage of having 78.646% more than what you contributed to your account by starting 15 years earlier, compared to having only accumulated 50.16% more than your total contributions by starting 15 years later.

Nelson Nash, the founder of the Infinite Banking Concept, repeatedly reminded those who listened, “Whole Life Insurance is designed to become more efficient every year, no matter what.” And because this is true, keeping your 10% in whole life insurance can be very rewarding for you and for future generations.

Nelson Nash, the founder of the Infinite Banking Concept, repeatedly reminded those who listened, “Whole Life Insurance is designed to become more efficient every year, no matter what.” And because this is true, keeping your 10% in whole life insurance can be very rewarding for you and for future generations.

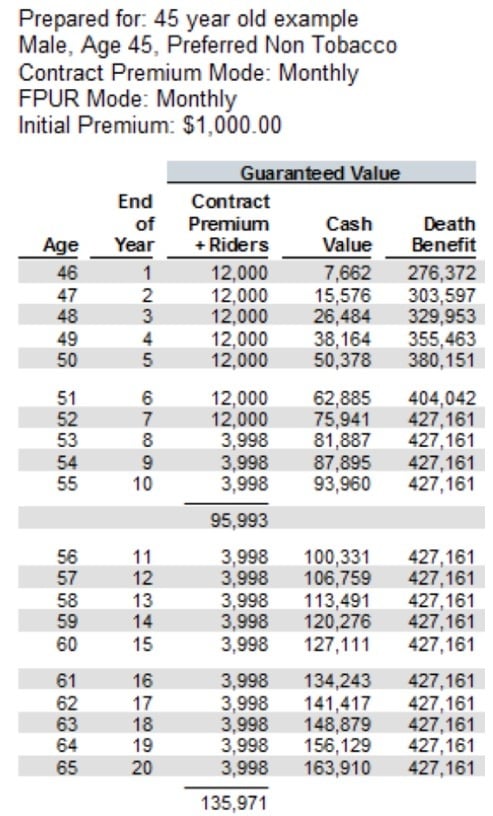

For an example of how Nash’s statement continues to hold true, examine the guaranteed values in the attached whole life insurance illustration.

In year 7, the premium paid for the year is $12,000 but the cash value increase for year 7 is guaranteed to be $13,056 (change from the previous year $75,941 – $62,885). This represents a cash value gain of 8.80% over the cost of the annual premium paid in year 7.

By year 20, the annual premium is no longer $12,000 but is only $3,998. And the guaranteed cash value increase for year 20 is $7,781.00 ($163,910 – $156,129). This represents a guaranteed cash value increase of 94.622% over the annual premium paid in year 20.

Considering guaranteed cash value increase from 8.80% over the annual cost of premium in year 7 to a guaranteed cash value increase of 94.622% over the annual cost for premium in year 20, ascertains Nash wasn’t fibbing when he said, “Whole Life Insurance is designed to become more efficient every year, no matter what.”

Because efficiency is guaranteed in whole life insurance, the rush to become a 401(k) or IRA millionaire by contributing more and more money to these non-guaranteed accounts becomes less desirable for those who recognize and appreciate the value of cash value in whole life insurance. There is little reason to expose your money to risk(s) when your money can accumulate risk free in guaranteed contracts.

This is why 100s of people have chosen to allow McFie Insuranceto design and service participating whole life insurance contracts for them to own and manage. At McFie Insurancewe care about you, your welfare, and your retirement. Call us at 702-660-7000. We are here to help you, your family and your friends keep more of the money you make, guaranteed.

Dr. Tomas P. McFie

Dr. Tomas P. McFie

Most Americans depend on Social Security for retirement income. Even when people think they’re saving money, taxes, fees, investment losses and market volatility take most of their money away. Tom McFie is the founder of McFie Insurance which helps people keep more of the money they make, so they can have financial peace of mind. His latest book, A Biblical Guide to Personal Finance, can be purchased here.