Schedule Appointment »

702-660-7000

702-660-7000

With high unemployment rates in the U.S., individuals are seeking access to savings accounts to sustain their family and/or business during the pandemic. Many are turning to their 401(k) retirement accounts as a financial safety net. Thanks to the CARES Act, many people can avoid the penalty and spread the 401(k) withdrawal tax over a three-year period.

If you’re thinking of withdrawing money from a 401k during these times, carefully consider the rules and regulations for an early 401(k) withdrawal under the CARES Act.

The 401(k) withdrawal tax is based on your income and tax bracket. However, you will be subject to a 401(k) tax penalty if you withdraw before the age of 59 1/2 . The penalty on an early 401(k) withdrawal is an extra 10%. During the COVID pandemic, the CARES Act has made early 401(k) withdrawals penalty free up to $100,000 for individuals affected by Coronavirus.

The CARES Act has temporarily eliminated the 10% early withdrawal and distribution penalty for 401k withdrawal and other qualified plan funds, up to $100,000. This law applies to you if you have been “affected” by the Coronavirus in one of these three ways:

Under these conditions, you can now access up to $100,000 as a penalty-free 401k withdrawal. This also applies to withdrawals from an IRA or 403(b). If you take a loan rather than a withdrawal from a 401(k) or 403(b), you can avoid the taxes as long as you pay the loan back in three years.

This new regulation affects nearly everybody who has an IRA, 401(k) or 403(b). And as just mentioned, even though the 10% penalty for early withdrawal from your IRA or distribution from your 401(k) has been removed, you will still have to pay the taxes on that money. To avoid this 401(k) tax, you can repay your qualified plan over the next three to five years.

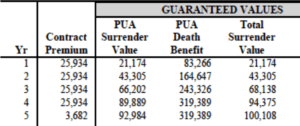

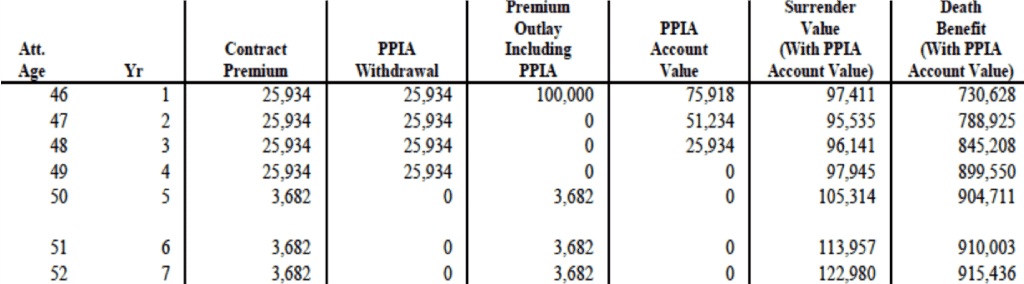

Obviously, you will have to pay the 401(k) taxes on that money regardless of when you take your money out, so here is a way to recover the 401(k) withdrawal tax over time so you don’t have to pay it later. This is your once in a lifetime chance to do so. (This illustration is on a healthy male age 45.)

These benefits cannot be accomplished with your IRA, 401(k), or 401(b). But they can with Whole Life insurance.

Penalty-free 401k withdrawals are certainly not an every-day occurrence. Now is the time if you wish to seize the opportunity of this “once in a lifetime chance” to avoid the 10% penalty and remove your money from the risk of the market. Start getting the guaranteed growth that mutual whole life insurance can legally provide for you.

Notice that $122,980 is the projected cash values for year 7 in this life insurance policy. That means you could completely recover the cost of the taxes you will have to pay on that $100,000 if you are in the 22% marginal tax bracket and decide NOT to pay the loan back. But here is some great news, the cash values in your life insurance policy will never be taxed again, if you follow the IRS guidelines.

The money you use to pay the principal and interest on your 401(k) or 403(b) loan (after the 5-year window) will be taxed before you pay your loan back AND it will be taxed again when you access that money in the future. This means double taxation on your same dollar!

You can only take an early withdrawal from an IRA, but you can borrow from your qualified plan, if your plan allows loans to be taken. The CARES Act merely waives the interest on loans taken from your qualified plan for 3 years at which time you will have to pay the loan back with interest, or it will be reclassified as an early distribution and you will have to pay the taxes owed.

If you already have an outstanding loan against your qualified plan, you may not be able to take another loan, depending on your employer’s plan loan guidelines. So be sure to check to see if you qualify.

Here’s the crux of the matter. Typical financial planning is telling people with IRAs, 401(k)s and 403(b)s to only take an early distribution or loan from your retirement account(s) as a last resort. But in contrast to typical advice, traditional financial planning encourages you to make sure that what you have earned is guaranteed and secure because traditional financial planning knows that you don’t have the time to accumulate that money all over again. Big losses are hard to recoup.

For example:

Traditional financial planning provides the protection you need for your money by using legally binding contracts which keep your money growing, safe and secure. No investment or deposit can even offer the same guarantees that you are automatically provided within participating whole life insurance. That is why traditional financial advice has always been to own participating whole life insurance as the foundation of your financial portfolio, because nothing else can compare.

Shopping for a well designed participating whole life insurance can be a time-consuming process. How do you know if the agent designing your policy knows how to include all the benefits and features you’ll want?

At McFie Insurancewe make the process easy because we know what options and benefits can be added to a policy as well as when and more importantly when not to add them. We’ll even show you how we design a good policy during a web meeting so that you can understand how the policy is built and ask questions as we go along.

If you want a good policy but don’t want to spend lots of time researching all the options for yourself we’ll happily share our knowledge with you and design a good policy for you. Click here to request a web meeting

Dr. Tomas P. McFie

Dr. Tomas P. McFie

Most Americans depend on Social Security for retirement income. Even when people think they’re saving money, taxes, fees, investment losses and market volatility take most of their money away. Tom McFie is the founder of McFie Insurance which helps people keep more of the money they make, so they can have financial peace of mind. His latest book, A Biblical Guide to Personal Finance, can be purchased here.