Many insurance agents market “7702 plans” as retirement vehicles, sometimes glossing over important details. This guide breaks down what IRC 7702 plans are, their benefits and drawbacks, and whether they’re right for your situation.

KEY POINTS

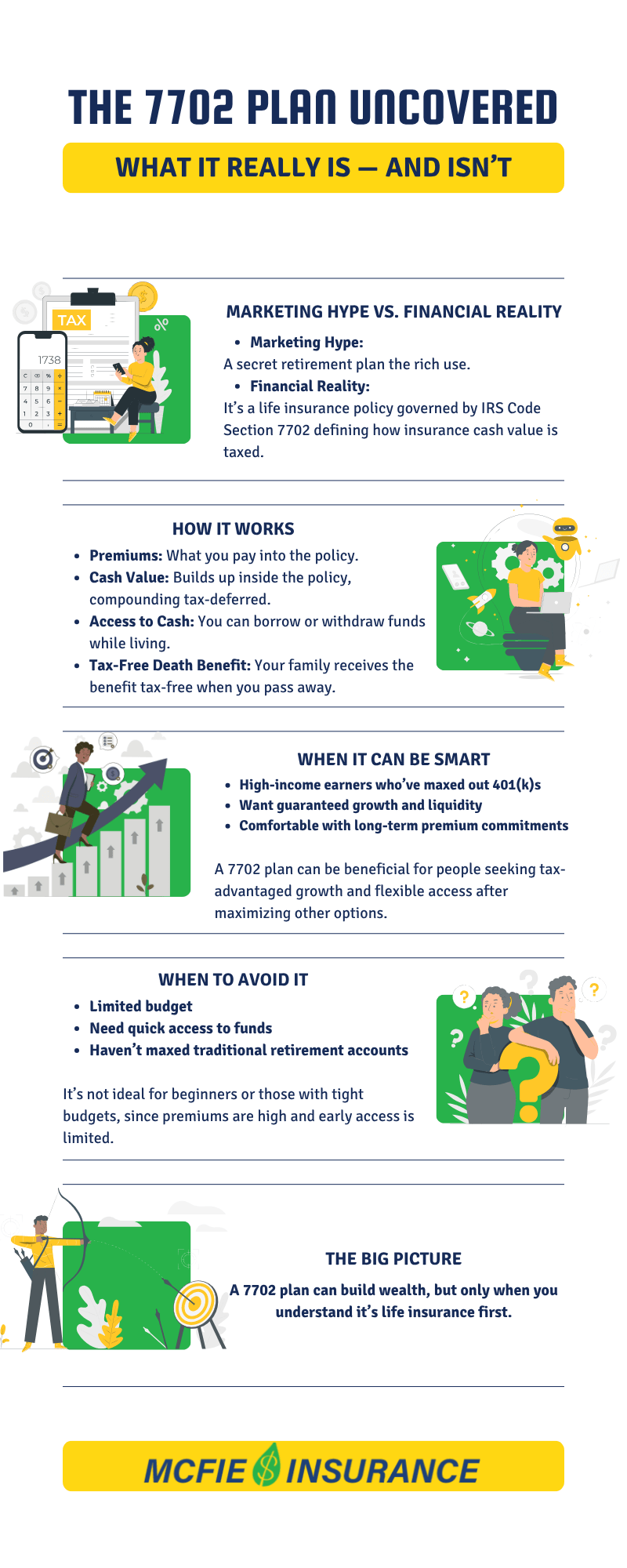

Nature of 7702 Plans: They are life insurance policies, not retirement plans, covered under Section 7702 of the Internal Revenue Code.

Benefits of 7702 Plans: These include tax-deferred cash value growth, tax-free loans or withdrawals, no contribution limits, consistent premiums, and tax-free death benefits.

Drawbacks of 7702 Plans: No tax deductions for contributions, potential surrender penalties, interest on policy loans, slow cash value growth, and high premium requirements.

Recent IRC 7702 Changes: In 2020, Congress amended Section 7702, affecting new life insurance products’ interest rates, leading to potentially higher premiums for similar cash values but not impacting existing policies unless significantly altered.

What Is an IRC 7702 Plan?

When you hear about a “7702 plan,” understand this isn’t a retirement plan at all, it’s a life insurance policy. The term “7702” refers to Section 7702 of the Internal Revenue Code (IRC), which governs how all life insurance policies are treated for tax purposes.

Some insurance agents use “7702 plan” terminology to sidestep mentioning life insurance upfront. However, there’s nothing wrong with life insurance when it’s properly designed to meet your needs.

An IRC 7702 plan is usually a cash-value life insurance policy with higher premiums than term insurance. When designed well, these higher premiums help you build cash value and overcome the cost of insurance faster.

How Does an IRC 7702 Plan Work?

An IRC 7702 plan functions exactly like a life insurance policy because that’s what it is. Here’s how it works:

Your premium purchases a death benefit while building cash value over time. After death, your beneficiary receives the death benefit from your policy. During your lifetime, you can access the cash value through withdrawals or policy loans from the insurance company. Think of cash value as your equity in the life insurance death benefit.

While it’s not accurate to call a 7702 plan a “retirement plan,” well-designed life insurance policies can provide advantages for retirement savings, offering options for more sustainable retirement income than typical financial planning that relies mainly on tax-deferred plans like 401(k)s and IRAs.

Whole Life Insurance Made Simple Instant Download

This free binder explains how Participating Whole Life Insurance (PWLI) works.

7702 Plans Compared to Traditional Retirement Accounts

Understanding the differences between 7702 plans and traditional retirement accounts is crucial:

7702 Plans (Life Insurance Policies):

Grow tax-deferred but premiums aren’t tax-deductible

No contribution limits

Access funds through loans or withdrawals

Main purpose is providing a death benefit

Can access money before age 59½ without IRS penalties

No required minimum distributions at age 72

Traditional 401(k) Plans:

Contributions are pre-tax, lowering taxable income

Annual contribution limits apply

Investment growth is tax-deferred

Specifically designed for retirement savings

10% penalty for withdrawals before age 59½

Required minimum distributions start at age 72

Both can be useful financial tools, but they serve different purposes and have different tax treatments.

Pros and Cons of 7702 Plans

Advantages of 7702 Plans

Tax-Deferred Growth of Cash Value The cash value in your policy grows without immediate tax implications, allowing your money to compound more effectively over time.

Tax-Free Access to Funds You can borrow against your cash value without triggering taxes. These policy loans aren’t classified as taxable income, giving you tax-free liquidity.

No Contribution Limits Unlike 401(k)s and IRAs with annual caps, there are no limits on how much you can contribute to a 7702 plan, making it attractive for high-income earners who’ve maxed out other retirement accounts.

Guaranteed Growth Unlike traditional investment portfolios that cannot guarantee returns, whole life insurance policies provide guaranteed growth on your money, offering confidence and financial peace of mind. Participating policies may also earn dividends based on the insurer’s performance.

Flexible Loan Repayment Policy loans don’t have repayment schedules or deadlines. You can repay at your own pace, and any outstanding loan balance can be offset by death benefit proceeds after your death.

Tax-Free Death Benefit Beneficiaries receive death benefits without owing income tax, providing valuable financial protection for your loved ones.

Consistent Premium Amount Premiums often remain level throughout the policy’s lifespan, making budgeting predictable.

No Required Minimum Distributions (RMDs) Unlike traditional retirement accounts, you’re not forced to take withdrawals at age 72, allowing your cash value to continue growing.

No Early Withdrawal Penalty Access your cash value before age 59½ without the 10% IRS penalty that applies to early withdrawals from retirement accounts.

Creditor Protection In many states, life insurance policies offer protection against creditors or bankruptcy, safeguarding your assets.

Easier Access to Funds You can borrow against it without credit checks, applications, or explanations.

Won’t Trigger Taxable Social Security Benefits Policy loans don’t count as income that could make your Social Security benefits taxable.

Disadvantages of 7702 Plans

No Tax Deduction for Contributions Premiums are paid with after-tax dollars, offering no immediate tax benefit unlike 401(k) contributions.

Extremely High Premiums Whole life insurance is initially more expensive than term life insurance because it develops a cash value.

Health-Based Eligibility You must qualify medically to obtain coverage. Poor health can result in higher premiums or denial of coverage entirely.

Utilizing IRC 7702 Plans Beyond Retirement

Besides offering a source of tax-free income in retirement, 7702 plans can aid in planning for expenses like college education, emphasizing the importance of early savings for such significant costs.

Section IRC 7702 Changes

In December 2020, Congress made changes to section 7702 for the first time since it was created 32 years before in 1988.

Through the Consolidated Appropriations Act, the minimum interest rates to be used in the design of cash-value life insurance products were changed to allow for continued low-interest rates across the rest of the economy.

Existing policy owners do not need to worry about their guaranteed policy values since these changes do not affect existing policy guarantees unless significant changes are made to an existing policy.

None of these changes negate the value of using whole life insurance/7702 plan as an important financial tool and a liquid form of savings in addition to the permanent death benefit.

Seeing the numbers from the insurance companies we represent here at McFie Insurance, we think the findings of the Society of Actuaries have been reflected pretty accurately across the industry resulting in:

higher guaranteed cash values;

higher premiums to support those cash values;

lower net amount at risk (less mortality risk);

premiums and dividends applied to buy paid-up additions would purchase less death benefit; and

less risk to the company in a sustained low-interest-rate environment.

Is a 7702 Plan Right for You?

IRC 7702 plans, while offering appealing benefits, might not be the best fit for everyone. However, you might find a 7702 plan advantageous if you:

Seek Additional Tax-Free Income in Retirement: If your goal is to increase your tax-free income during retirement.

Have Maxed Out Other Retirement Contributions: If you’ve already reached your contribution limits in your 401(k) or other qualified retirement plans and are looking for further tax-advantaged growth.

Desire Principal Protection in Various Market Conditions: If you want to safeguard your principal regardless of stock market fluctuations.

Wish to Access Benefits While Alive: If you’re interested in a plan that allows you to use certain benefits during your lifetime.

Prefer Not to Recover Losses Before Gaining Again: If you want to avoid the necessity of making up for losses before seeing gains.

Seek Financial Security with a Death Benefit: If having a death benefit for financial coverage in unexpected situations is important to you.

Want to Avoid Taxable Social Security Benefits: If you’re concerned about additional income making your Social Security benefits taxable.

Prefer No Mandatory Withdrawals Post-Age 72: If you don’t want to be obligated to withdraw funds at age 72, nor face penalties for not doing so.

Summary

An IRC 7702 plan is not a retirement plan. It’s a section of the internal revenue code that dictates how life insurance will be treated for tax purposes. Some experts say life insurance is the single largest benefit in the tax code. Thanks to section 7702, life insurance is not just effective for providing financial protection for your loved ones when you die, it is also a great way to grow your wealth while you’re alive.

It can provide retirement income for you in your golden years and it lets you leave money to your spouse, your children, and your grandchildren income tax-free! With a better understanding of the IRC 7702 pros and cons, you can make more informed decisions about your life insurance for your financial success.

Whole Life Insurance Made Simple Instant Download

This free binder explains how Participating Whole Life Insurance (PWLI) works.

To see the numbers for a well-designed life insurance policy/7702 plan and how this could benefit you, call McFie Insurance at 317-912-1000 or schedule a time for us to call you.

by John T. McFie I am a licensed life insurance agent, and co-host of the WealthTalks podcast.

As a 16-year practitioner of the Infinite Banking Concept on a personal level, I can help you find the clarity and peace of mind about your financial strategy that you deserve. Working with hundreds of financial scenarios over the years has helped me to develop a sixth sense about how to quickly find a clear and balanced solution for clients using whole life insurance as a financial tool.