Schedule Appointment »

702-660-7000

702-660-7000

If retirement is your goal, you want to start preparing and saving as soon as possible. However, you’ve probably heard of more than one way to save for retirement. Two common retirement plan options are investing in a 401(k) or using a whole life insurance policy. Many people wonder if a whole life insurance policy or a 401(k) is a better choice for preparing for retirement.

While both 401(k)s and whole life insurance can be used to create a viable retirement plan, there are still pros and cons for each. In this article, we’ll evaluate whole life insurance vs. a 401(k) and determine which is better for your unique financial situation.

401(k) plans and life insurance are two distinct financial tools designed for securing future finances, each serving unique purposes and potentially being part of a retirement strategy.

Employer-managed 401(k) plans are dedicated retirement savings plans. Participating employees allocate a portion of their income to these plans, contributing to their retirement fund.

Life insurance, in contrast, primarily ensures financial security for the policyholder’s beneficiaries after their passing. Policyholders pay premiums to maintain their coverage, which is largely focused on providing a death benefit. Some life insurance types also incorporate an investment aspect, which could aid in retirement savings.

A 401(k) is typically a feature of an employee benefits package offered by companies, where employees contribute a part of their salary to their retirement account.

Life insurance differs as it primarily provides financial protection for beneficiaries in case of the policyholder’s death, helping to manage significant expenses like a mortgage. While the cash value from permanent life insurance can supplement retirement savings, it is not usually recommended as a primary retirement plan, unlike a 401(k) or similar plans.

| 401(k) Plan | Whole Life Insurance |

|

|

Using a 401(k) as a retirement plan is a common approach to retirement savings. According to the Census Bureau, approximately 32% of Americans have a 401(k). These retirement plans are offered through many employers and can be a simple way to start saving while you’re working full-time. Here are some of the pros and cons of a 401(k) as a retirement plan.

A 401(k) is typically managed through your employer.

Most often, an employer will have a system in place where you choose to opt into a 401(k) plan and contribute a certain amount of your paycheck each pay period. This method makes it easy to contribute to your retirement savings once the plan is in place. The other main benefit is that many employers offer to contribute to your 401(k) as well. Some employers will match your contributions—up to a certain established amount—which can help increase your savings in your 401(k) without draining any more of your paycheck.

You can usually move your 401(k) when you switch employers.

You won’t have to worry about losing your savings if you switch jobs, as long as you’re fully vested in the contributions. A 401(k) is a way to save with small amounts at a time, either regularly or erratically so it can be an easily affordable plan.

Taxes

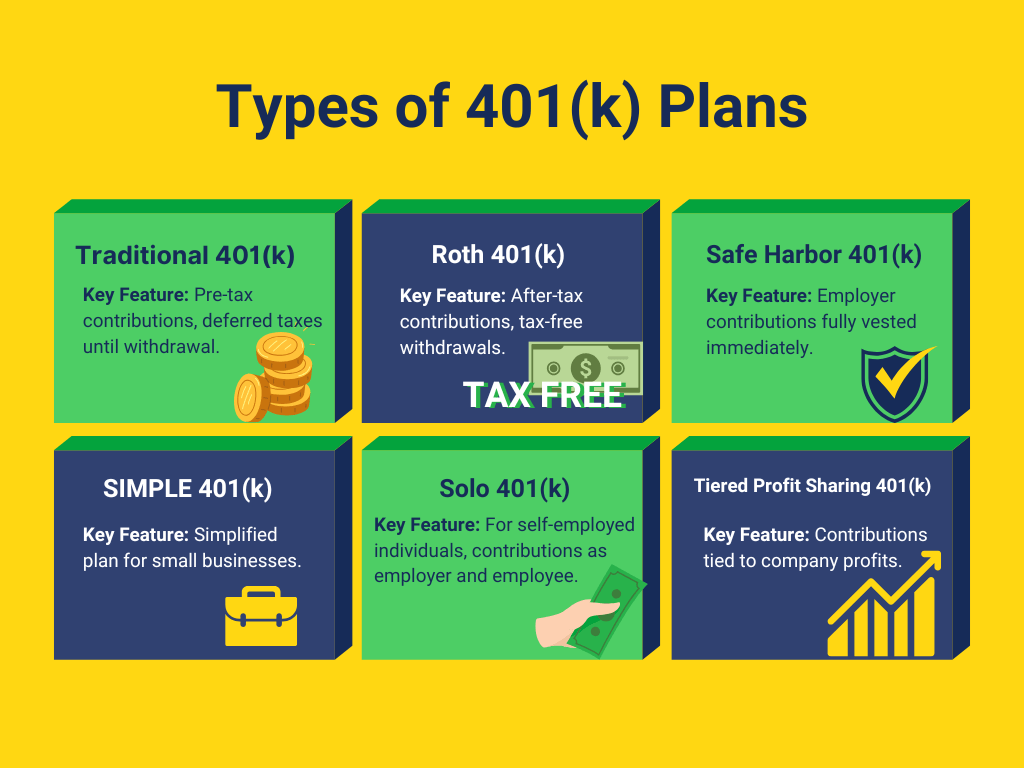

As with most things, 401(k)s can be tricky to work out the taxes and to make sure you’re still saving enough money post-taxation. There are two kinds of 401(k)s: Traditional and Roth. With a traditional 401(k) you don’t pay taxes on the savings until you withdraw it, at which point, it’s taxed as normal income.

You probably see why this can be dangerous. You may see that you’ve saved a certain amount. Then when you take from that savings and it’s taxed, you’re left with an amount that looks quite different.

If you choose a Roth 401(k), you pay taxes on your contributions regularly each year. Upon withdrawal, taxes are only paid on employer contributions and the growth associated with those contributions. No further taxes are paid on your contributions and all the growth on your contributions over the same time.

Withdrawing from a 401(k) can be difficult.

You must satisfy certain conditions to be able to withdraw money from a 401(k) plan. Most plans require you to be 59 ½ years old and/or meet a few other criteria before you can access the money. While this does prevent you from spending it, you aren’t able to access the money you’ve accumulated in an emergency or to use for your financial legacy without a penalty.

Whole life insurance isn’t explicitly a retirement plan, but it can be used as part of a retirement plan to great success. Essentially to use a life insurance retirement plan (LIRP), you should purchase a well-designed whole life insurance plan and use it to accumulate cash value. The cash value you accumulate over your working life can then be used to fund your retirement at the right time. The advantage of using whole life insurance over other life insurance options is that whole life offers better guarantees and strong cash value growth.

You can save for retirement and still have a death benefit.

Other retirement plans can help you save up the necessary funds to retire, but they don’t provide you with the security of a death benefit at the same time. Whole life insurance does provide a death benefit while also helping you accumulate cash value that you can use for retirement.

The cash value your whole life insurance policy accumulates is available to you now.

You can take loans against your policy values and use these dollars to fund necessary expenses, paying the loan back at your convenience. If you’re ever in a situation where you need to access emergency funds, you’re able to access that account at whatever age and without meeting conditions that 401(k)s require.

The fact that life insurance cash value is accessible during your working years can allow you to save more than you would wish to save in a 401(k) where you can’t get to the money for several years.

Being able to access the cash value of your life insurance policy and savings also means that you’re able to use the plan now to begin cultivating your financial legacy. You can build a legacy to leave behind to benefit your posterity.

Premiums can be higher than 401(k) contributions limits.

This is not a factor for everyone, but some high-income earners are not able to save as much as they want for retirement through a 401(k) because of contribution limits. Whole life insurance premiums do not have contribution limits imposed by tax rules. The only limit is how much life insurance the insurance companies will approve for you, primarily based on income and net worth.

Premiums are also the main disadvantage of whole life insurance.

The premiums for a whole life policy may be higher than what you’re contributing to a 401(k) or the initial premiums for term insurance, and they’re not quite as flexible as making contributions to a 401(k) whenever you have the money.

The premiums cause some people to hesitate before getting a whole life insurance policy because they’re worried about the affordability. However, these premiums allow you to accumulate cash value (retirement savings) and a death benefit simultaneously.

Access to the cash values building in whole life insurance via policy loan can be used to help with premiums as needed. Although this is not a good long-term strategy, it does provide much better short-term flexibility than most people realize.

Deciding between life insurance and a 401(k) can be challenging due to the unique benefits each offers. However, you don’t always have to choose one over the other.

Combining life insurance with a 401(k) can enhance your overall financial strategy. Owning a permanent life insurance policy provides access to cash value, useful for various needs. This complements the retirement savings built up in your 401(k), leading to a more sturdy financial plan.

A 401(k) and a whole life insurance policy can work as retirement plans. A 401(k) provides tax deductions right now, a whole life insurance plan can be more financially beneficial long term.

Using both whole life insurance and a 401(k) plan is sometimes a good option as well. Many people contribute just enough to a 401(k) to get the full employer match and then stash extra money into a whole life insurance policy where they can still access the cash value.

Some people ask about whole life insurance in a 401(k) plan. This can be an option for some people, but there are several rules which make this difficult and we usually find it better to buy a whole life insurance policy outside a 401(k) plan. When it comes to long-term benefits, guarantees, and flexibility, whole life insurance offers all of these features. If you’re unsure what type of life insurance would be best for your situation, schedule a free strategy consultation with our experts. We can help you figure out the best way to use life insurance to start saving more for your retirement today.

Related Posts:

How Much Should You Have in Your 401(k)?

Avoid the 401(k) Withdrawal Tax Under The Cares Act

by John T. McFie

by John T. McFie

I am a licensed life insurance agent, and co-host of the WealthTalks podcast.

As a 15-year practitioner of the Infinite Banking Concept on a personal level, I can help you find the clarity and peace of mind about your financial strategy that you deserve.

Working with hundreds of financial scenarios over the years has helped me to develop a sixth sense about how to quickly find a clear and balanced solution for clients using whole life insurance as a financial tool.

This free binder has the information to build your own Infinite Banking system.