Schedule Appointment »

702-660-7000

702-660-7000

by Ben McFie

The Infinite Banking Concept (IBC) or infinite banking life insurance is outlined in the book Becoming Your Own Banker by R. Nelson Nash. My introduction to infinite banking life insurance was on a family vacation to San Diego, California in 2005. I was only 12 years old when my Dad was reading the book Becoming Your Own Banker, and he was so excited about what he was reading that he was having me and my older brother, who was 14 at that time, sit and listen to excerpts from the book as he read.

To be honest, I would have rather been on the beach than sat in the condo listening to Dad read a financial book to us, but at the same time, I was excited because I saw that Dad was excited. My Dad is a Doctor of Chiropractic. At that time, he owned a chiropractic clinic in Oregon. He was in practice long before I was born.

But it was on that vacation, and specifically the message in that book, Becoming Your Own Banker, that changed the course of our family’s life forever. Here’s an introduction to the Infinite Banking Concept and how McFie Insurance (formerly Life Benefits) got started.

The founder of the Infinite Banking Concept, R. Nelson Nash, served in the United States Air Force, worked as a forestry consultant and later became a life insurance agent and a real estate investor. To get money for his real estate investments prior to the 1980s, Mr. Nash was accustomed to paying 9.5% on the money he borrowed. But in the early 1980s, interest rates on the money he owed jumped to 23%! In his book he wrote, “There I stood owing $500,000 under those circumstances.”

According to Mr. Nash, “The basic idea revealed in the Infinite Banking Concept was born over a period of many, many months at 3am to 4am in the kneeling position praying ‘Lord please, show me a way out of this financial nightmare that I have created for myself.’” He writes, “The answer came back about like a baseball bat across the eyes…You can get to money during these awful times, at 5% to 8% from three different life insurance companies through policies that you own. The only thing that limits how much you can get to is the same thing they tell you at the bank when you ask them how big of a check you can write – how much have you put in?’”

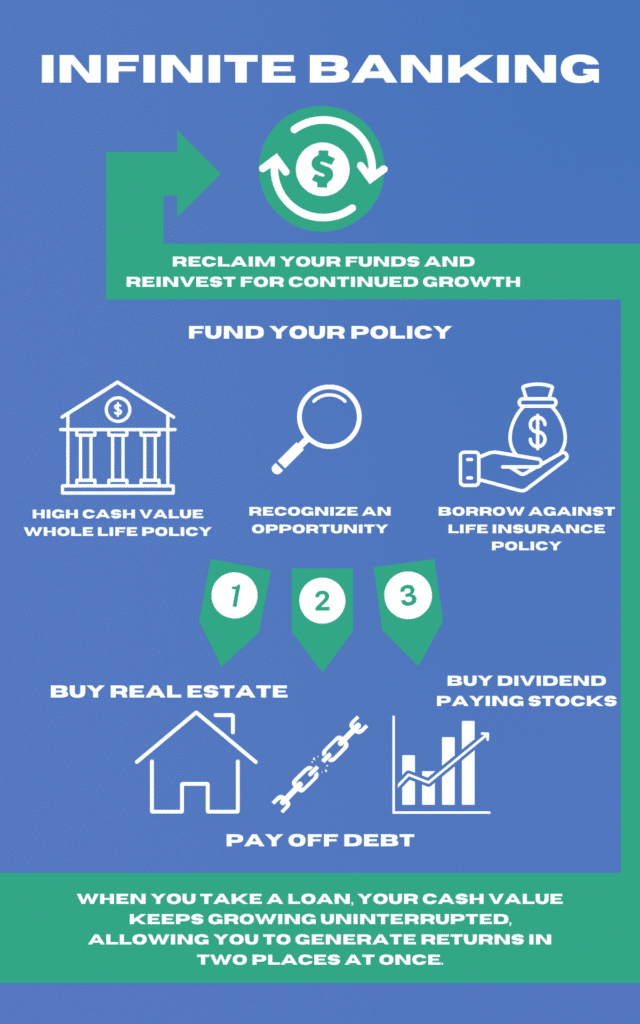

But exactly what is infinite banking life insurance? The Infinite Banking Concept is basically the idea that by funding one or more properly designed dividend-paying Whole Life insurance policy(ies), you will have guaranteed access to cash that you can leverage for anything you choose.

When we got home from vacation, Dad dug out the term life insurance policies he owned to see if they were convertible to Whole Life Insurance. Unfortunately, they weren’t. But he met with someone who designed a dividend-paying Whole Life insurance policy like Mr. Nash described in his book.

|

Infinite Banking Made Simple Instant Download This free binder has the information to build your own Infinite Banking system. |

Soon, Dad was on the phone telling family and friends about the Infinite Banking Concept. During the week, in his clinic, he would also tell his patients about the book and share the concept with them too. A few months later, he decided to get his life insurance producer’s license, so he could design, sell, and service Whole Life insurance policies.

Over the next few years, Dad provided education about the Infinite Banking Concept to so many people that he retired from chiropractic and sold his clinic so that he could spend more time teaching about infinite banking life insurance. But it wasn’t just Dad’s business. Mom was working alongside him, and even as teenagers, we started helping however we could.

If you’ve researched very much about the Infinite Banking Concept, there’s a good chance you know my Dad as Dr. Tom McFie. You may have even read one of his books or seen one of his video presentations on YouTube. In fact, if you don’t already have it, you can get his most popular book, Prescription for Wealth, as a free digital download. The forward to Prescription for Wealth was written by Mr. Nash himself.

Things have changed over the last several years. The Infinite Banking Concept is still around, and it still works. Mr. Nash’s son-in-law, David Stearns, still runs the company Infinite Banking Concepts, which among other things, sells the book Becoming Your Own Banker. Before Mr. Nash died, an institution for certifying agents was formed by Nelson Nash, David Stearns, and two other men, Carlos Lara, a consultant from Tennessee, and Robert P. Murphy, a senior economist at the Independent Energy Institute.

The institution, now called the Nelson Nash Institute, was formed after the Infinite Banking Concept was facing serious danger from the life insurance profession. Will the institution protect the brand by defining what the Infinite Banking Concept is and certifying Infinite Banking Practitioners? Time will tell. You can read my Dad’s thoughts on that here.

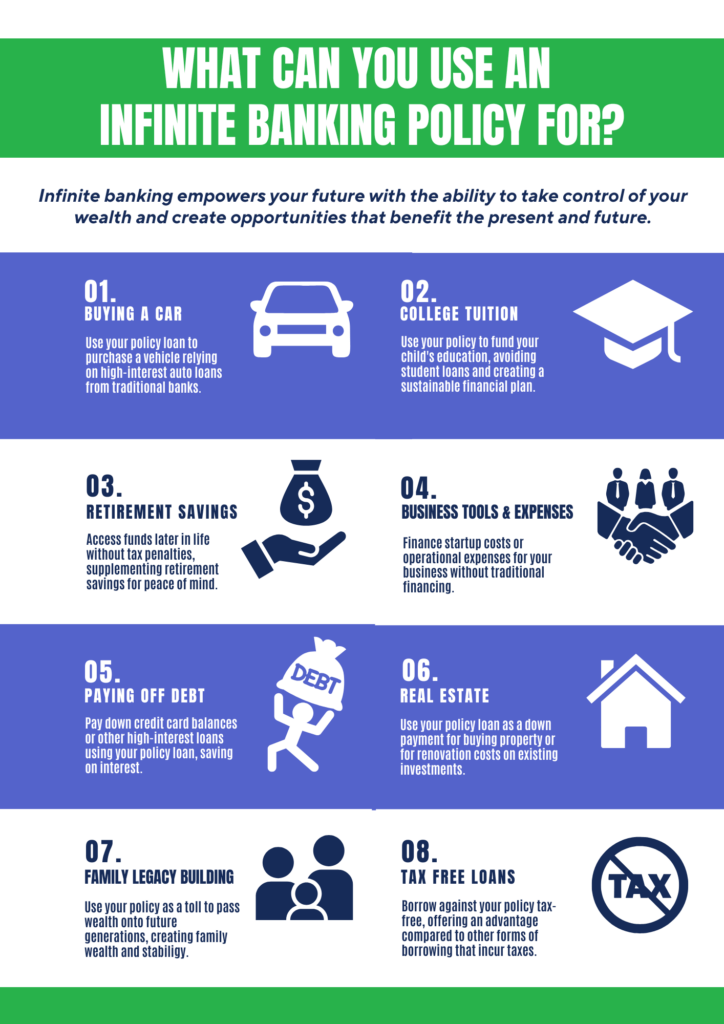

Infinite Banking is “infinite” because the ways you can use the concept are infinite. This concept leverages the cash value of whole life insurance policies as a personal banking system.

The Infinite Banking Concept is a process, and the ways it can be used are infinite, it has been adapted to many different situations already and it will be adapted to many more as people use their creativity to apply the process to an infinite number of financial situations.

Today, there are many different programs with different names that share the same root idea of using a good dividend-paying Whole Life insurance policy to build a source of guaranteed available capital that you can manage and use for whatever you choose. Here is a list, by no means exhaustive, of other similar programs that utilize the root idea of the IBC:

At the end of the day, you will find that any of these programs are only as good as the people behind them…whether it’s the person inventing it, marketing it, or teaching it.

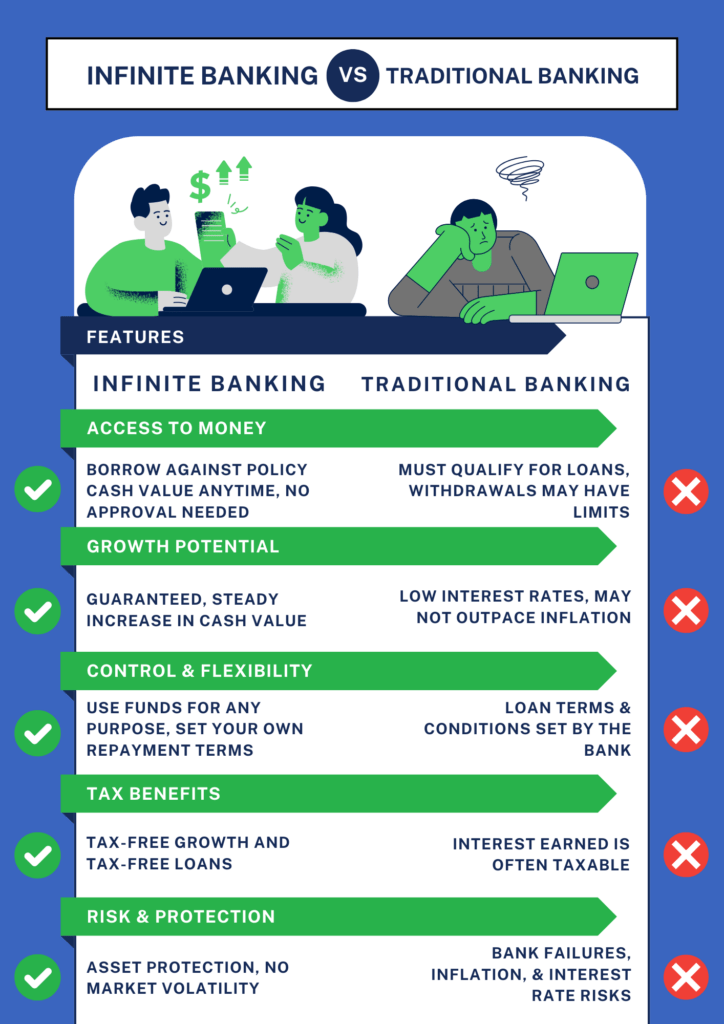

A good Infinite banking policy will have cash value that continues to grow even if you take a policy loan. This is an obvious benefit that is not available with most traditional savings vehicles.

Policy loans can be taken against the cash value of an infinite banking policy. Policy loans are signature loans and are not subject to approval like a traditional loan would be.

The growth in a good infinite banking policy is tax deferred.

Infinite banking is primarily about using the life benefits of a life insurance policy while you’re alive, namely the cash value, but there is also a death benefit associated with an infinite banking policy and the death benefit provides financial peace of mind simultaneously.

Depending on your state’s laws, Infinite banking policy values can receive protection from creditors.

Policy loans don’t appear on credit reports.

You won’t have access to the amount of money you have used to fund your policy for the first few years. Even though you will likely have access to more money than you have used to fund your infinite banking policy in the future, it takes a few years to get to that point.

An infinite banking policy will need regular premium payments for at least the first 7 years.

Not everyone can buy a life insurance policy for infinite banking because you must qualify for coverage to be able to buy a policy.

are all taken into account by the underwriters at the insurance company. At McFie Insurance we help people go through the “underwriting process” to qualify for life insurance policies they can use for infinite banking.

One of the biggest problems people can have with infinite banking is changing their financial habits when necessary. People who don’t save money are the ones who experience this problem.

We’ve noticed over the years that there are certain groups of people who find Infinite Banking especially valuable:

Business Owners

Seem to understand the power of putting their money to work in multiple ways.

Real Estate Investors

Like to have money available at a moment’s notice and the cash value of an infinite banking policy checks that box.

People Who Save Money

Are saving money with the future in mind, they understand the long game and know the value of a good whole life insurance policy that is designed to have excellent guaranteed growth.

People Planning for Retirement

Want to have retirement funds they can count on and they want tax preferred treatment without penalties or required distributions. You can get all of that with good whole life insurance.

The short answer is the infinite banking concept is legitimate but it has been used as a scam also.

Life insurance agents have used Infinite Banking as a life insurance sales system but they don’t always design the life insurance policies they sell to work well for infinite banking. This is basically a scam because people who think they are buying a policy that will work for infinite banking end up with a policy that won’t work for infinite banking at all!

As you can see, it’s not a problem with the concept itself, but rather a problem with people who don’t have good character.

If a policy is designed well for Infinite Banking it will have:

If a policy is not designed well for Infinite Banking it might

Policy design is critical to having a policy that works well for Infinite Banking.

You can borrow against:

These loans might even have lower interest rates than a policy loan.

But here’s what makes whole life insurance different:

If you borrow against market involved assets, you’re at the mercy of changing markets. But with life insurance, you have control and certainty.

You can borrow against stocks but you’re limited to about 50% of their value, compared to about 95% with whole life insurance. Plus, when market prices fall your borrowing power falls too.

Bonds let you borrow between 50-75% of their value. But they face challenges when interest rates change, and they can lose value during market volatility – exactly when you might want access to your money most.

A home equity line of credit might seem like a good option. But HELOCs aren’t guaranteed to always be available. Banks can reduce them or close them.

401(k) loans have several limitations:

While each of these options can serve a purpose, none offer the reliability and consistent access you get with a well-designed whole life insurance policy.

As the Infinite Banking Concept caught on, more and more people began to want dividend-paying Whole Life insurance policies. Life insurance agents around the country began to take note. Some agents loved the idea, some agents loved the thought of using the idea as a sales system to sell more life insurance. This created a problem. To design a good policy that works well for the Infinite Banking Concept, you have to minimize the base insurance in the policy and increase the paid-up insurance rider. It’s not hard to do, but commissions are paid directly in relation to how much base insurance is in the policy. So, cutting down the base policy also cuts an agent’s commission.

Some agents are willing to cut their commission to design a good policy for the customer, but many agents are not. Unfortunately, many life insurance agents told their customers that they were writing an “Infinite Banking Policy” but ended up writing them a bad Whole Life insurance policy, or even worse, some type of Universal Life insurance policy, whether it was a Variable Universal Life insurance policy or an Indexed Universal Life insurance policy.

The Infinite Banking Concept started to get a bad name, in fact, a very popular Google search used to be, “Is the infinite banking concept a scam?” Many people were getting a bad taste in their mouths about the Infinite Banking Concept because they were getting bad policies.

Another threat to the concept came because some life insurance agents started calling life insurance policies “banks”. This language caught the attention of some state regulators and restrictions ensued.

Individuals and businesses can benefit from infinite banking life insurance. Dividend-paying Whole Life insurance is readily available and can be designed to maximize cash value and minimize the death benefit, just like Mr. Nash described in his book Becoming Your Own Banker. The challenge is finding the right agent who is willing to design a good policy, teach you how to use it correctly, and remain available to help you with your policy.

|

Understanding the Infinite Banking Concept and How It Works In Our Modern Environment 31-page eBook from McFie Insurance Order here> |

The internet is your friend, and your enemy, because the right and the wrong, the good and the bad, the true and the false, and everything else in between is right in your face. As always, use discernment and heed this advice from Abraham Lincoln.

If you are interested in infinite banking life insurance and are in the market to get a good policy, I’m biased, but I recommend our family’s company, McFie Insurance. Not only have we specialized in setting up good policies for use with the Infinite Banking Concept for over 16 years, but we also own and use the same type of policies personally. If you like our educational materials and are comfortable with our recommendations, please consider working with us. You can schedule a free strategy session with us to get started.

If you already have policies, or you are currently working with another agent, you can get what is called an independent insurance review. An independent insurance review is where another life insurance professional looks over your policy, or illustration, and provides you with a report. Depending on where you get your insurance review, the review may be free or you may have to pay. Either way getting a second opinion can be invaluable. Our family’s company, McFie Insurance, offers an independent insurance review free of charge. Contact us today if you’re interested in making sure your policy is well-designed and working for you in the right ways.

If you are interested in infinite banking life insurance and are in the market to get a good policy, I’m biased, but I recommend our family’s company, McFie Insurance. Not only do we specialize in setting up good policies for use with the Infinite Banking Concept but we also own and use the same type of policies personally and we have for over 18 years. We offer a free appointment for people who want to see what an infinite banking policy would look like for them, ask questions and find out if they want to work with us. We are licensed in all 50 states.

If you already have policies, or you are currently working with another agent, you can get what is called an independent insurance review. An independent insurance review is where we look at your policy, or illustration, and review it for you. We charge $75 to do an independent insurance review. It is well worth the $75 to have financial peace of mind.

Whole Life insurance is still the premier financial asset. It provides guaranteed growth, options, certainty, liquidity, and tax benefits…all with zero market risk. It limits tax risk, hedges against inflation, and lets you pass on wealth tax-free when you die.

Whether the Infinite Banking Concept continues to exist as a brand or not, our family keeps Mr. Nash’s idea alive. It’s a brilliant idea. It helps people keep more of the money they make, grow their wealth, and have financial peace of mind.

We teach individuals, business owners, and families, in all 50 states, how to use dividend-paying Whole Life insurance to create exponential wealth. I don’t see that changing anytime soon.

Whether you’re interested in learning more about infinite banking life insurance or looking to start using the concept with your own policy, contact us to schedule a free strategy session.

Ben T. McFie

Ben T. McFie

There's a lot of confusion around finance; there's so much to know and it's frustrating when you don't know enough to make the best financial decisions. I like to bring clarity to financial matters so people can make good financial decisions that will help them live wealthier more fulfilling lives.

This free binder has the information to build your own Infinite Banking system.