Schedule Appointment »

317-912-1000

317-912-1000

Bank-Owned Life Insurance (BOLI) is a financial strategy used by banks to strengthen their long-term stability. In a typical BOLI arrangement, the bank is both the owner and the beneficiary of the policy. This allows the institution to take advantage of the policy’s tax-advantaged cash value growth—an effective way to offset the rising cost of employee benefits.

These policies aren’t issued for every employee. Instead, they’re reserved for top executives or key board members—those whose sudden absence could cause a meaningful financial disruption to the institution. Upon the death of one of these individuals, the death benefit is paid directly to the bank.

It’s important to note: BOLI isn’t a benefit for the employee. It’s a strategic asset the bank uses to protect itself. While this may sound impersonal, it’s common practice among large financial institutions because of the financial efficiencies it creates.

If banks recognize the long-term financial strength of whole life insurance for their own portfolios, maybe it’s time individuals start paying attention too.

When a bank implements Bank-Owned Life Insurance (BOLI), it often does so through a structure known as an “insurance trust.” This trust functions like a specialized financial reservoir. The bank makes regular premium payments into the trust, and the policy is typically tied to the life of a key executive.

Over time, the policy’s cash value grows—tax-deferred—and can be used to help offset the rising cost of employee benefit obligations. When benefits need to be paid, the bank draws from this trust, not from its day-to-day operating funds.

One of the biggest advantages? The growth within the BOLI trust is generally tax-free, making it a highly efficient strategy for funding long-term liabilities. While most individuals will never be offered a BOLI policy, they can benefit from the same financial principles that make whole life insurance such a powerful tool—even for the banks.

If banks are using life insurance to preserve and grow wealth, maybe it’s worth considering for your own financial future.

The U.S. Department of the Treasury’s Office of the Comptroller of the Currency (OCC) provides guidance for the purchase of BOLI policies. They allow banks to buy such policies for various reasons, including to recover costs of offering employee benefits, insuring key personnel, and more. The OCC is also open to considering other uses of BOLI on an individual basis.

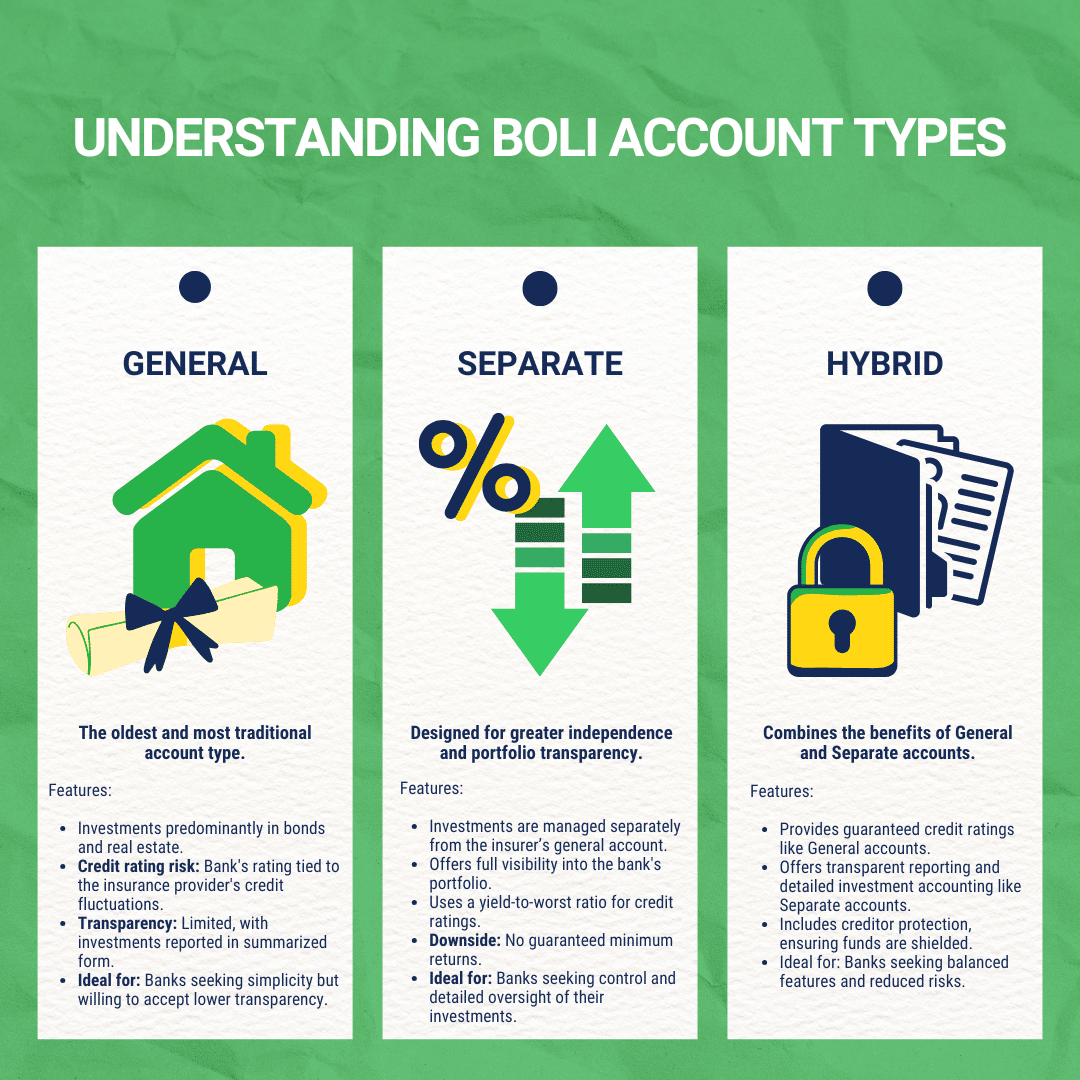

Banks have three primary BOLI options: general, hybrid, and separate accounts.

The increasing trend of BOLI integration with benefit plans for top-tier executives. More banks are exploring BOLI to balance out their employee benefit expenses.

Advantages: BOLI offers tax advantages, helps offset costs associated with employee benefits, and retains its value even if the insured employee parts ways with the bank.

Disadvantages: If a bank needs to surrender a BOLI policy, potential tax implications and penalties can arise. The creditworthiness of the BOLI insurance provider is also crucial, especially since BOLI is not a liquid asset.

Banks use Bank-Owned Life Insurance (BOLI) as both a tax shelter and a strategic funding tool for employee benefit plans. The premiums they pay and the growth of the invested capital inside these policies are generally tax-free—making BOLI a smart financial move for large institutions.

When a covered executive passes away, the bank receives a tax-free death benefit. These policies are not designed to protect families—they’re designed to protect the bank’s bottom line.

Bank-Owned Life Insurance, as the name suggests, is a specialized insurance product tailored exclusively for banks and large corporations. As a result, the general public, including individual consumers, cannot access or purchase BOLI for their own or family’s financial planning. BOLI is strategically designed to meet the unique needs of banks, primarily to fund employee benefit plans and to secure tax advantages.

This doesn’t mean individuals are left without life insurance options. A plethora of life insurance products exist in the market, each tailored to suit the specific needs of individuals and families. From term life insurance, which offers protection for a specific number of years, to whole life insurance, which provides lifelong coverage and builds cash value, there are a myriad of choices available. It’s essential for individuals to consult with financial advisors or insurance agents to understand which policy best aligns with their financial goals and protection needs.

Policy Checklist

Policy Checklist

Make Sure You Get a Good PolicyIs your policy good or bad? Use this checklist to help evaluate your existing life insurance or a new policy you are considering.

The presence of BOLI in the market is expanding steadily, a testament to its growing importance in the banking sector. As of June 30, 2023, the collective cash surrender value of BOLI policies held by banks reached an impressive $202.4 billion, as reported to the FDIC. This significant figure underscores the critical role BOLI plays in bank finance strategies and risk management.

Several reasons contribute to this uptick in BOLI adoption among banks:

With these benefits and the continued growth of the banking sector, BOLI’s market presence is poised to expand even further. It’s worth noting that while BOLI plays a vital role in a bank’s strategy, it also demands careful management to ensure compliance with regulations and to maximize its advantages.

Understanding the Infinite Banking Concept and How It Works In Our Modern Environment 31-page eBook from McFie Insurance Order here>

The increasing adoption of BOLI by banks is a testament to its efficacy as a tax shelter and a funding tool for employee benefits. By safeguarding the interests of high-value employees and board members, banks can utilize the policy’s proceeds to offset benefit schemes. BOLI offers a competitive edge to banks in the realm of employee benefits, ensuring both the institution’s and its employees’ welfare, provided the chosen insurer upholds robust credit standards.

If you would like to learn more about BOLI reach out to the team at McFie Insurance to help you better understand how to use life insurance as an asset.

Ben T. McFie

Ben T. McFie

There's a lot of confusion around finance; there's so much to know and it's frustrating when you don't know enough to make the best financial decisions. I like to bring clarity to financial matters so people can make good financial decisions that will help them live wealthier more fulfilling lives.

This free binder has the information to build your own Infinite Banking system.