When it comes to estate planning and protecting your assets, trusts are often touted as powerful tools. But not all trusts are created equal. The two main categories – revocable and irrevocable trusts – have some key differences that you need to understand before deciding if either is right for your situation.

At McFie Insurance, we believe in empowering our clients with knowledge so they can make informed decisions about their finances and legacy. That’s why we’re tackling this complex topic head-on. Let’s dive into the details of revocable and irrevocable trusts, examining the pros and cons of each, and why we generally advise caution when it comes to irrevocable trusts.

A revocable trust, also known as a living trust, is a flexible estate planning tool that allows you to maintain control of your assets during your lifetime. As the name suggests, you can revoke or modify this type of trust at any time. Here’s what you need to know:

Key Features of Revocable Trusts:

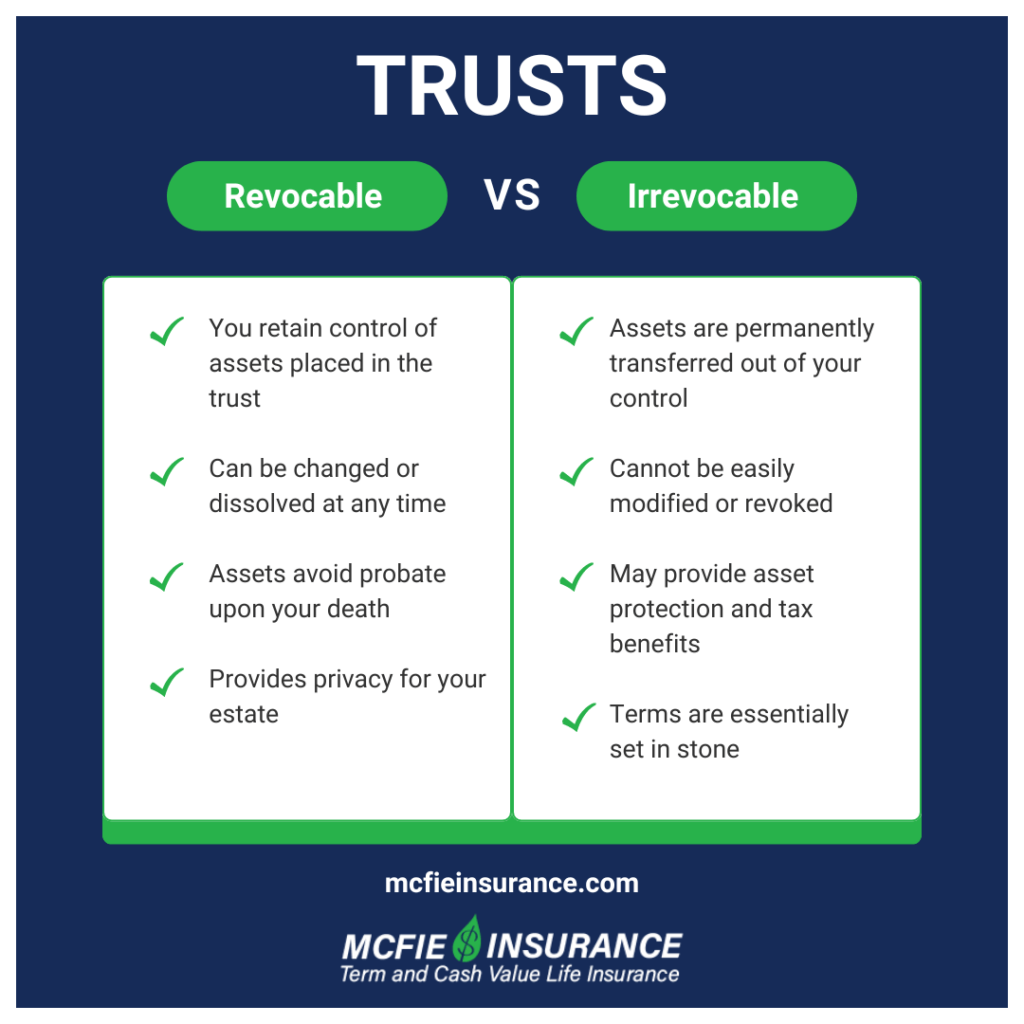

You retain control of assets placed in the trust

Can be changed or dissolved at any time

Assets avoid probate upon your death

Provides privacy for your estate

Advantages of Revocable Trusts:

Flexibility: Life is unpredictable, and your financial needs may change over time. A revocable trust allows you to adapt as circumstances evolve. You can add or remove assets, change beneficiaries, or even dissolve the trust entirely if needed.

Probate Avoidance: Assets properly transferred to a revocable trust avoid the time-consuming and potentially expensive probate process. This can save your heirs significant hassle and expense.

Privacy: Unlike a will, which becomes public record during probate, a revocable trust keeps your affairs private. The terms of the trust and the assets it contains remain confidential.

Continuity of Management: If you become incapacitated, your designated successor trustee can step in to manage the trust assets without court intervention. This ensures smooth management of your affairs even if you’re unable to do so yourself.

Disadvantages of Revocable Trusts:

No Asset Protection: Because you retain control of the assets, a revocable trust does not protect against creditors or legal judgments. The assets are still considered part of your estate.

No Tax Benefits: A revocable trust does not provide any income tax or estate tax advantages. The assets are still considered part of your taxable estate.

Ongoing Management: You’ll need to actively manage the trust, ensuring assets are properly titled and the trust is kept up to date. This requires some ongoing effort and potentially professional assistance.

Initial Setup Costs: Creating a revocable trust typically involves higher upfront legal fees compared to a simple will. However, this cost may be offset by avoiding probate expenses later.

The Other Side: Irrevocable Trusts

An irrevocable trust, as the name implies, cannot be easily changed or revoked once established. This permanence is both its greatest strength and its most significant drawback. Here’s what you should understand:

Key Features of Irrevocable Trusts:

Assets are permanently transferred out of your control

Cannot be easily modified or revoked

May provide asset protection and tax benefits

Terms are essentially set in stone

Advantages of Irrevocable Trusts:

Asset Protection: Because you no longer own the assets in an irrevocable trust, they may be protected from creditors and legal judgments against you personally.

Potential Tax Benefits: Properly structured irrevocable trusts can provide estate tax benefits by removing assets from your taxable estate. Some types may also offer income tax advantages.

Medicaid Planning: In some cases, irrevocable trusts can be used as part of a strategy to qualify for Medicaid while preserving some assets for heirs.

Charitable Giving: Certain types of irrevocable trusts can be effective tools for charitable giving, potentially providing tax benefits while supporting causes you care about.

Disadvantages of Irrevocable Trusts:

Loss of Control: This is the big one. Once assets are placed in an irrevocable trust, you no longer own or control them. The trustee manages the assets according to the trust terms, and you can’t simply change your mind later.

Inflexibility: Life circumstances, tax laws, and family dynamics can all change dramatically over time. An irrevocable trust may not be able to adapt to these changes, potentially leaving you with an outdated and ineffective strategy.

Complexity and Cost: Irrevocable trusts are often more complex to set up and administer than revocable trusts. This can mean higher legal and accounting fees, both initially and ongoing.

Potential for Unintended Consequences: Because of their permanence, poorly designed irrevocable trusts can lead to family conflicts, unforeseen tax issues, or other problems that can’t be easily corrected.

Why We Urge Caution with Irrevocable Trusts

We believe in empowering our clients to maintain control of their finances and legacy. That’s why we generally advise caution when it comes to irrevocable trusts. Here’s why:

The Permanence Problem: The very feature that makes irrevocable trusts attractive for asset protection – their permanence – is also what makes them potentially dangerous. Once you’ve placed assets in an irrevocable trust, you’ve given up control. If your circumstances change or you simply have a change of heart, you’re largely out of luck.

Unintended Consequences: We’ve seen too many cases where well-intentioned individuals set up irrevocable trusts, only to regret it years later. Maybe family dynamics shifted, tax laws changed, or financial needs evolved in unexpected ways. The inflexibility of an irrevocable trust can leave you stuck with an arrangement that no longer serves your best interests.

Complexity and Costs: Irrevocable trusts often require ongoing professional management and advice to ensure they’re administered properly and continue to meet legal and tax requirements. This can be a significant ongoing expense that eats into the value of the trust over time.

Loss of Financial Control: Irrevocable trusts, by their very nature, require you to give up a significant degree of control. This goes against our philosophy of empowering individuals to be their own bankers and money managers.

Alternative Strategies Available: In many cases, the goals people hope to achieve with irrevocable trusts can be accomplished through other, more flexible means. Whether it’s asset protection, tax planning, or leaving a legacy, there are often strategies that don’t require the permanent loss of control that comes with an irrevocable trust.

When Might an Irrevocable Trust Make Sense?

While we generally advise caution, there are situations where an irrevocable trust might be appropriate. These tend to be specific circumstances where the benefits clearly outweigh the significant downsides:

Large Estates Facing Estate Taxes: For individuals with estates well above the federal estate tax exemption (currently $12.92 million for individuals in 2023), an irrevocable life insurance trust (ILIT) or other specialized trusts might be worth considering as part of a comprehensive estate tax strategy.

Special Needs Planning: In some cases, an irrevocable special needs trust can be an effective way to provide for a disabled loved one without jeopardizing their eligibility for government benefits.

Asset Protection for High-Risk Professions: Individuals in professions with high litigation risk (e.g., surgeons) might consider an asset protection trust, but only after careful consideration of all alternatives and potential downsides.

Certain Charitable Giving Strategies: Some irrevocable charitable trusts can provide tax benefits while supporting causes you care about. However, these should be approached carefully and with expert guidance.

The McFie Insurance Approach: Flexibility and Control

We advocate for strategies that allow you to maintain flexibility and control over your financial future. That’s why we often recommend alternatives to irrevocable trusts that can achieve similar goals without the permanent loss of control:

Properly Designed Whole Life Insurance: A well-structured whole life insurance policy can provide tax-advantaged growth, accessible cash value, and a tax-free death benefit for heirs. Unlike an irrevocable trust, you maintain control of the policy and can access its value during your lifetime.

Revocable Living Trusts: For many individuals, a revocable living trust provides sufficient estate planning benefits (probate avoidance, privacy, incapacity planning) without the drawbacks of an irrevocable trust.

Strategic Use of Limited Liability Entities: For business owners and real estate investors, properly structured LLCs or other entities can provide asset protection without the need for irrevocable trusts in many cases.

Maximizing Retirement Accounts: Prudent use of retirement accounts like 401(k)s and IRAs can provide tax advantages and some degree of asset protection without giving up control of your assets.

Education and Ongoing Financial Management: Providing education for our clients and helping them actively manage their finances is often the best “asset protection” strategy. Knowledgeable, engaged individuals are better equipped to navigate financial challenges and opportunities.

Policy Checklist Make Sure You Get a Good Policy

Is your policy good or bad? Use this checklist to help evaluate your existing life insurance or a new policy you are considering.

When it comes to estate planning and asset protection, there’s no one-size-fits-all solution. Revocable trusts offer flexibility but limited asset protection, while irrevocable trusts provide stronger protection at the cost of control and flexibility. For most individuals, the loss of control that comes with an irrevocable trust is too high a price to pay.

Before making any decisions about trusts or other estate planning tools, it’s crucial to thoroughly understand your options and how they align with your specific goals and circumstances. We encourage you to seek advice from qualified professionals who can provide a comprehensive view of your situation.

Remember, the goal isn’t just to protect your assets – it’s to create a financial strategy that allows you to live your best life now while also providing for your loved ones in the future. By maintaining control and flexibility, you’re better positioned to adapt to life’s changes and opportunities.

If you’d like to learn more about how we approach estate planning and asset protection at McFie Insurance, we invite you to schedule a strategy session with us. We’ll help you explore all your options and develop a plan that gives you the control and peace of mind you deserve.

Tomas P. McFie DC PhD

Tom McFie is the founder of McFie Insurance and co-host of theWealthTalks podcast which helps people keep more of the money they make, so they can have financial peace of mind. He has reviewed 1000s of whole life insurance policies and has practiced the Infinite Banking Concept for nearly 20 years, making him one of the foremost experts on achieving financial peace of mind. His latest book,A Biblical Guide to Personal Finance, can be purchased here.

This free binder has the information to build your own Infinite Banking system.