Schedule Appointment »

702-660-7000

702-660-7000

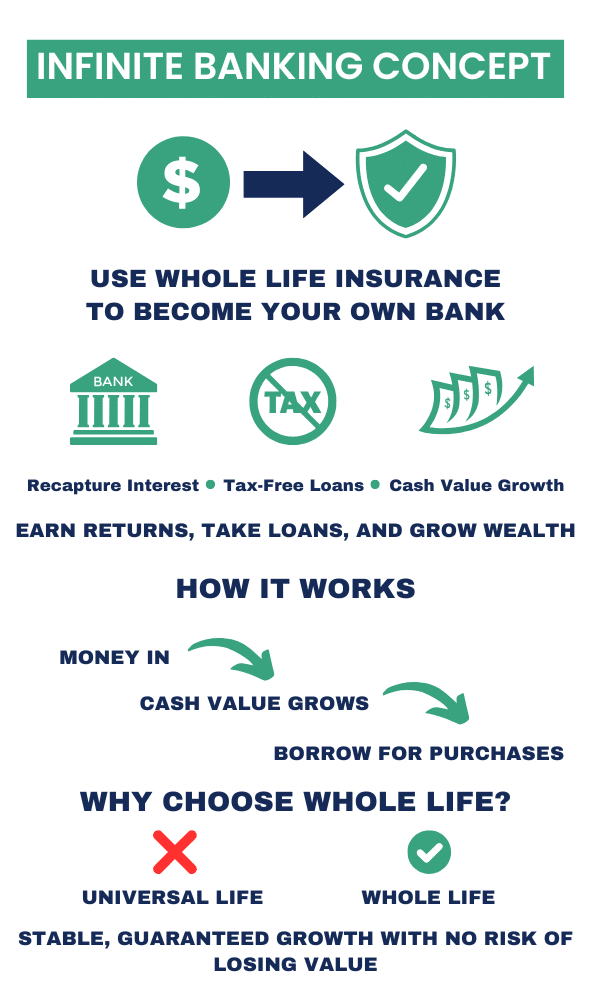

Nelson Nash developed the Infinite Banking Concept (IBC) in the 1980s as a strategic financial approach that allows individuals to recapture interest they would otherwise pay to banks, build cash value in a secure financial vehicle, and create a lasting legacy through life insurance. This concept emerged during a period of extraordinarily high interest rates when Nash, struggling with his highly leveraged real estate investments, discovered he could access capital from his whole life insurance policies at 5-8% while banks were charging up to 23% interest.

In his book “Becoming Your Own Banker,” published in 1999, Nash outlined a system that transformed what began as a personal solution for high-interest debt into a financial strategy. The concept is built around three principles:

What many fail to understand about traditional loans is the difference between interest rate and volume of interest. For example, a $250,000 mortgage at 5% APR over 30 years results in paying over 48% of your total payments as interest. If you refinance after just 5 years (as many Americans do), this volume increases to 75% because most interest is paid during the early years of amortized loans. The Infinite Banking Concept addresses this wealth transfer by keeping more of this interest within your financial system.

Not all life insurance policies are created equal when it comes to implementing the Infinite Banking strategy. A properly designed policy for IBC should:

When designed correctly, a policy can achieve 50-70% of first-year premiums as accessible cash value, with this percentage improving over time. Well-designed policies see guaranteed cash values exceed total premiums paid between years 8-15. With the addition of dividends (which, while not guaranteed, have been paid by many mutual companies for over 100 years), the performance improves further.

The cash value in a whole life policy represents your equity in the death benefit, similar to equity in a home. This creates an essential distinction from universal life insurance policies. In whole life, cash value is not a separate side account but rather the portion of the death benefit that is fully paid up and owned by the policyholder.

This cash value grows in two ways: through guaranteed increases built into the policy contract and through dividends declared by the insurance company. When you borrow against your policy, you’re using the insurance company’s money (from their general account) while your cash value grows uninterrupted within the policy. This is different from withdrawing the money, which would reduce your cash value and slow your policy’s growth.

Policy loans form the heart of the Infinite Banking Concept. Unlike traditional loans, policy loans do not require credit checks or a qualification process, making access to funds seamless. There is no fixed repayment schedule, giving borrowers flexibility in managing their finances. Policyholders can use the loan for any purpose without restrictions, and their full cash value continues to grow, though with direct recognition companies, the loan may impact dividends. Policy loans also provide tax-free access to capital as long as the policy remains in force. When used for business or investment purposes, they may even offer tax deductions.

While there is always a cost to policy loan interest (typically 5-8% depending on the company and loan structure), the value comes from maintaining control of your capital, earning returns on your money, and recirculating funds within your personal banking system rather than having them flow to external financial institutions.

Understanding the differences between whole life insurance and various universal life products is essential for implementation of the Infinite Banking Concept:

Universal Life Insurance (including Indexed and Variable):

Nash explicitly warned against using universal life products for IBC, noting these policies “kept ‘falling apart’ when the insured attained age 65-70” because “the cost of the one-year term became prohibitive at the advanced ages and ‘ate up the cash fund’ from that point forward.”

Mutual life insurance companies have demonstrated exceptional stability throughout American financial history. During the Great Depression, only 20 of 350 life insurance companies went into receivership, while over 4,000 banks failed. Even during the 2008 financial crisis, policy values remained secure while many other financial instruments experienced dramatic losses.

This stability stems from several factors:

Many mutual insurance companies have paid dividends for over 100 years, even through world wars, the Great Depression, stagflation, and recent financial crises.

The Infinite Banking Concept isn’t focused on earning the highest possible returns but rather on creating a system of disciplined capital accumulation and deployment that you control. This perspective aligns with how successful business owners view their finances.

Jeff Bezos, in his 2004 letter to Amazon shareholders, stated: “Our ultimate financial measure is free cash flow…” This focus on free cash flow rather than profits has been central to Amazon’s growth strategy. Similarly, IBC practitioners prioritize financial control, flexibility, and sustainability over chasing the highest returns.

The practical applications of the Infinite Banking Concept extend to endless financial situations:

Debt Management: Rather than focusing solely on paying off debt quickly, IBC practitioners often find better results by maintaining disciplined payments while building their banking system. This approach creates more flexibility and better long-term results.

Major Purchases: By financing cars, equipment, or other major purchases through your banking system, you recapture the interest that would otherwise go to third-party lenders.

Business Financing: Using policy loans for business capital allows entrepreneurs to maintain control and flexibility while creating tax advantages through properly structured interest payments.

Investment Opportunities: Having liquid capital available allows investors to act quickly when opportunities arise, especially during market downturns when traditional financing may be restricted.

Retirement Income: The tax advantages of policy loans can create efficient retirement income streams without triggering tax events or required minimum distributions.

Estate Planning: The death benefit provides an efficient wealth transfer mechanism that avoids probate and can be structured to minimize estate taxes.

Many successful businesspeople throughout American history have used this approach:

In the modern corporate world, many major companies use a similar strategy called Corporate-Owned Life Insurance (COLI) to fund employee benefits, manage executive compensation, and provide balance sheet stability. Companies like Bank of America, Wells Fargo, JP Morgan Chase, Walmart, and Comcast have billions in cash value life insurance on their books.

Despite its long history of successful implementation, the Infinite Banking Concept faces several common misconceptions:

“It’s too good to be true” – The benefits of IBC don’t come from magical returns but from financial discipline, recapturing interest, and leveraging the tax and legal advantages of life insurance structures.

“Whole life insurance is a bad investment” – Whole life insurance isn’t designed to be an investment but rather a financial tool providing multiple benefits. Comparing it solely on rate of return misses the broader value proposition.

“You’ll earn more in the market” – While market investments may produce higher nominal returns in some periods, they come with volatility and risk. IBC provides stability, guarantees, tax advantages, and control that market investments cannot match.

“You can just use a bank for the same purpose” – Traditional banks don’t offer the same combination of tax advantages, uninterrupted compound growth, death benefit, and control found in properly structured whole life insurance.

The Infinite Banking Concept has created a paradigm shift in how people think about money, banking, and wealth creation. By understanding and implementing the principles of becoming your own banker through whole life insurance, individuals can create a financial system that offers greater control and long-term sustainability than conventional financial approaches.

This isn’t a get-rich-quick scheme, but rather a disciplined approach to building sustainable wealth by recapturing interest payments, maintaining control of your money, and establishing a financial legacy. With proper implementation and patience, this strategy can help you keep more of the money you make and build financial security for generations to come.

As with any financial strategy, implementation details matter significantly. Working with knowledgeable professionals who understand the insurance products and the Infinite Banking Concept is essential for prime results. The strategy’s power comes not from any single transaction but from the systematic application of the principles over decades, creating compounding benefits that extend beyond the original policyholder to future generations.

Tomas P. McFie DC PhD

Tomas P. McFie DC PhD

Tom McFie is the founder of McFie Insurance and co-host of the WealthTalks podcast which helps people keep more of the money they make, so they can have financial peace of mind. He has reviewed 1000s of whole life insurance policies and has practiced the Infinite Banking Concept for nearly 20 years, making him one of the foremost experts on achieving financial peace of mind. His latest book, A Biblical Guide to Personal Finance, can be purchased here.

This free binder has the information to build your own Infinite Banking system.