Schedule Appointment »

702-660-7000

702-660-7000

The headlines made it sound like a financial miracle: “Woman saves $7,800 a year on groceries by couponing!” At first glance, it seems like a success story in frugality. But when you dig a little deeper, the math tells a different story.

A South Carolina woman recently gained media attention for slashing her weekly grocery bill from $200 to just $50 through extreme couponing. That’s a remarkable 75% reduction in weekly spending on food. Inspired by the television show Extreme Couponing, she’s made bargain hunting her full-time project—spending Monday through Friday tracking down the best coupon deals available in her area.

What the headlines didn’t emphasize is the cost of chasing those savings. To achieve that $7,800 in annual grocery savings, she reports traveling more than 300 miles per week. That’s over 15,600 miles per year solely dedicated to coupon runs.

Now, consider the cost of driving those miles. According to the American Automobile Association (AAA), the average cost of driving a car—including gas, maintenance, insurance, depreciation, and other expenses—is about 60.8 cents per mile. When you do the math:

300 miles/week x $0.608 = $182.40/week

$182.40/week x 52 weeks = $9,484.80/year

So, while she saves $7,800 on groceries, she’s spending nearly $9,500 annually on driving to get those deals. That’s a net loss of over $1,600 per year. Even if she were driving a highly efficient electric vehicle, which averages about 54.3 cents per mile, the cost would still total around $8,469 per year—still outpacing the grocery savings.

The takeaway? It’s important to look beyond the surface of flashy savings headlines. While couponing can reduce grocery costs, it shouldn’t come at the expense of hidden costs that outweigh the benefit. True financial efficiency considers savings and the cost of achieving them.

That said, the woman in question also works weekends at Red Lobster as a server. According to the U.S. Bureau of Labor Statistics, the average hourly wage for a server in a casual dining restaurant—tips included—is about $11.73 per hour. That means if she picked up just 13 more hours per week at her job, she would earn more income than she’s saving by driving all over town hunting for coupons. But of course, working more hours isn’t “free” either. It comes at the cost of time, energy, and quality of life.

The point here isn’t to discourage bargain hunting. Many people today are wise to search for deals and avoid overpaying. There’s nothing wrong with being a smart shopper. But sometimes, chasing the perfect deal becomes a cycle—more like a dog chasing its own tail—costing you more in resources than the savings are worth.

There’s a popular saying: “Everyone knows the price of everything but the value of nothing.” And that sentiment hits home when it comes to extreme bargain hunting. At a certain point, your time, mental energy, wear and tear on your vehicle, and even strain on your relationships are worth more than shaving off a few extra pennies from a purchase.

Years ago, we subscribed to a newsletter called The Tightwad Gazette—a favorite among frugal living advocates. But it didn’t take long to realize that running from store to store to save ten cents was often more expensive than simply paying the ten cents extra at the store five minutes away. The effort was admirable—but not always efficient.

This same principle applies to shopping for life insurance. Yes, you should never overpay. But just like with bargain hunting, delaying the actual purchase of life insurance while you “shop around” can be a costly mistake. If your health changes or if rates increase, that delay could mean paying more—or worse, becoming uninsurable altogether.

In both bargain hunting and financial planning, it’s not just about what you spend—it’s about what you lose when you’re focused only on cost. Sometimes, the smarter move is to act with confidence and timeliness, rather than chase elusive savings that come at a greater cost.

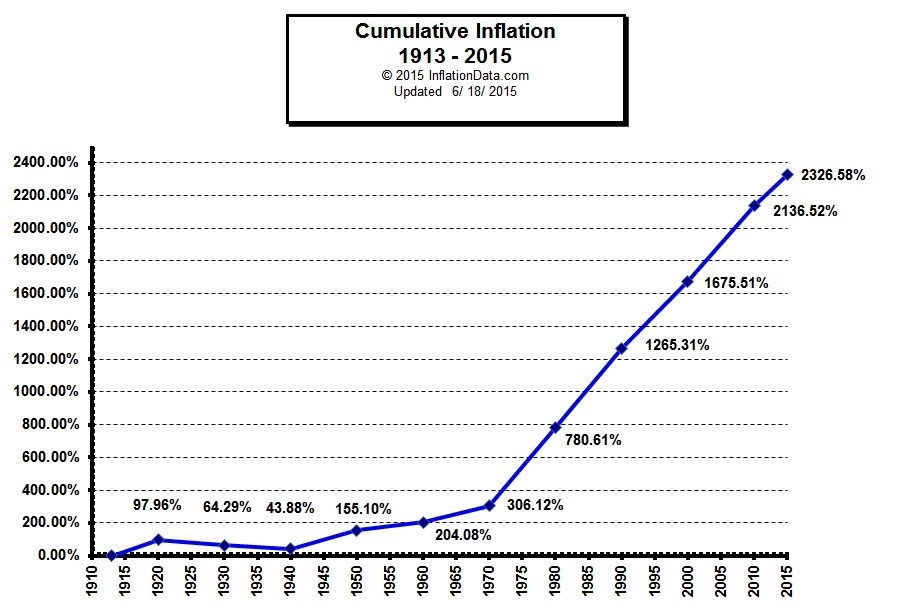

The time value of money is one of the most important financial principles to understand. It demonstrates that when your money isn’t growing—when it’s not earning compound interest in your favor—its purchasing power is actually declining. Inflation silently chips away at your wealth over time. Since 1913, when the Federal Reserve took over control of the U.S. dollar, inflation has averaged around 3.22% per year. That may not sound like much on the surface, but the cumulative effect is staggering. A single dollar in 1913 had over 2,300 times more purchasing power than a dollar in 2019. That’s the impact inflation has had on the value of our currency.

What does this mean for you today? It means that letting your money sit idle, or delaying financial decisions while you endlessly research or wait for the “perfect deal,” can cost you far more in lost growth than you might realize. To make the most of your financial future, keep these takeaways in mind:

Do your research, but don’t get stuck in decision paralysis. Comparing options is smart, but waiting too long can destroy the future value of your money. The longer your dollars stay unproductive, the more you lose to inflation and missed opportunity.

Factor in the value of your time. Time is a finite resource. Sometimes the money you save from bargain-hunting is eclipsed by the time and energy it costs to find those savings. In many cases, your time is worth more than the dollars you’re trying to stretch.

Be cost-conscious with life insurance, but not short-sighted. Don’t pay more than you need to—but also don’t assume that cheaper is better. Some policies might seem affordable upfront, but end up costing you more over time in lost benefits or coverage gaps. Work with a knowledgeable advisor to make sure you’re getting value and protection for your money.

Understand the difference between price and value. Just because a product or policy is advertised as a deal doesn’t mean it’s a good one. A bargain is only a bargain if the quality holds up. Before you chase after savings, make sure the product or service you’re getting is worth it.

Don’t stress about getting the absolute lowest price every time. Yes, it’s wise to be financially mindful. But don’t let that mindset dominate your life. At a certain point, it’s okay to say, “This is good enough.” Your peace of mind, relationships, and daily happiness are worth far more than the last dime you could’ve saved.

In the end, it’s not just about dollars—it’s about time, quality, and intention. You can always earn more money, but you can never create more time. Spend both wisely.

Tomas P. McFie DC PhD

Tomas P. McFie DC PhD

Tom McFie is the founder of McFie Insurance and co-host of the WealthTalks podcast which helps people keep more of the money they make, so they can have financial peace of mind. He has reviewed 1000s of whole life insurance policies and has practiced the Infinite Banking Concept for nearly 20 years, making him one of the foremost experts on achieving financial peace of mind. His latest book, A Biblical Guide to Personal Finance, can be purchased here.

This free binder has the information to build your own Infinite Banking system.