Schedule Appointment »

702-660-7000

702-660-7000

For decades, the American dream of retirement has centered around a simple formula: contribute to your 401(k) and IRA during your working years, become a millionaire, and enjoy a comfortable retirement. This strategy was first introduced in 1974 with tax-deductible IRAs, followed by 401(k) plans in 1978. Despite decades of promotion as the ideal path to retirement security, the results have been disappointing.

According to the Federal Reserve Survey of Consumer Finances, only 3.2% of U.S. retirees have managed to accumulate $1 million or more in their retirement accounts. Even more concerning is the question that haunts even those successful few: “Will a million dollars be enough to last my entire lifetime?”

This article will explore why retirement vehicles like 401(k)s and IRAs often fall short of their promises and how participating whole life insurance offers an alternative with unique benefits that these typical retirement accounts can’t match.

The retirement industry has spent decades promoting the idea that diligent saving in tax-advantaged accounts will lead to a comfortable retirement. Yet the data tells a different story.

Let’s consider a hypothetical retiree who has successfully reached that coveted million-dollar mark in their retirement accounts. If they need $60,000 annually to maintain their lifestyle, they’ll need to withdraw about $75,000 each year when accounting for taxes. This guarantees that they have enough after-tax income to cover their expenses.

Using historical market return data, this million-dollar nest egg would be depleted in 16 years. That’s without even factoring in the management fees, trading costs, and other expenses associated with 401(k)s and IRAs, which would reduce this timeframe even further.

This presents a problem when we consider life expectancy. According to the Social Security Administration, a 65-year-old man today can expect to live an additional 16.95 years on average, while a woman of the same age has a life expectancy of 19.75 more years. Those in above-average health can expect to live even longer. The math doesn’t work in favor of many retirees.

Let’s examine how most Americans are saving:

To accumulate $1 million over a 40-year career with this annual contribution, you would need to consistently earn a 4.87% annual return. Only 3.2% of retirees have managed to reach this milestone. This low “batting average” should give us pause.

Even those who diligently save face another challenge: liquidity. According to Lending Tree, nearly half (49%) of Americans don’t have enough savings to cover even a minor $1,000 unexpected expense. This lack of accessible funds means that even those who are building retirement assets may find themselves vulnerable to financial emergencies that could derail their long-term plans.

While 401(k)s and IRAs offer some tax advantages, they come with restrictions that limit their flexibility:

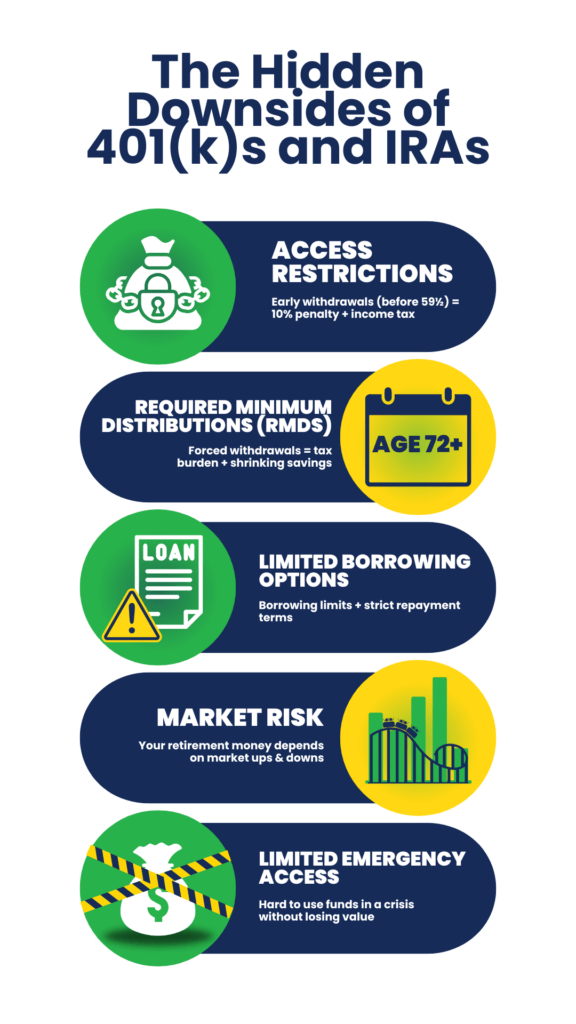

The government strictly controls when and how you can access your money. Withdrawals before age 59½ incur a 10% penalty plus income tax on the withdrawn amount. While some exceptions exist for hardships or first-time home purchases, these are limited and subject to specific criteria.

Once you reach age 72 (73 for those turning 72 after December 31, 2022), you must begin taking required minimum distributions from most retirement accounts, regardless of whether you need the money. This forced liquidation can create tax issues and reduce the longevity of your savings.

While some 401(k) plans allow loans, these come with strict limitations:

Your retirement security depends heavily on market performance, especially during the years immediately before and after retirement. A market downturn at the wrong time can reduce your retirement income potential.

When unexpected expenses arise, accessing retirement funds often means penalties, taxes, and permanent reduction of your retirement assets.

Participating whole life insurance (PWLI) offers a distinctly different approach to long-term financial planning that addresses many of the shortcomings of traditional retirement accounts.

When funded at the same $8,549 annual rate as the average 401(k) contribution, a participating whole life insurance policy can generate over $1 million in cash value over a 40-year period, alongside a death benefit of at least $1.6 million.

But the true advantage lies in how this financial tool functions during your lifetime:

Unlike retirement accounts, the cash value in a whole life policy can be accessed at any time through policy loans. These loans can be used for any purpose without restriction – whether it’s covering an emergency, funding education, starting a business, or seizing an investment opportunity.

The policyholder has complete control over repayment terms. Since policy loans are technically collateralized by the death benefit (not the cash value itself), the cash value grows uninterrupted in the policy, even while borrowed funds are being used elsewhere.

The flexibility of whole life insurance is one of its greatest strengths:

Whole life insurance offers significant tax benefits:

Unlike market-based retirement accounts, participating whole life insurance provides:

One of the most powerful aspects of participating whole life insurance is how it allows you to use your money multiple times through what some call the “velocity of money.” When you borrow against your policy to make purchases or investments, your underlying cash value continues to grow as if you hadn’t borrowed a cent.

This means you can:

This concept is often described as “having your cake and eating it too.” Imagine if you could recover all the money spent on cars, education, homes, appliances, and vacations throughout your life, while still enjoying those purchases. Would running out of money in retirement still be a concern?

When comparing traditional retirement accounts to participating whole life insurance, it’s important to look beyond the return percentages and consider the total financial picture:

The traditional retirement account path comes with constraints that limit its effectiveness. Contributions are capped annually and further restricted based on income levels, while growth remains vulnerable to market volatility and economic downturns. Access to these funds before retirement triggers penalties, and once retirement arrives, required minimum distributions force withdrawals regardless of your financial needs. Withdrawals generally face taxation, creating an additional burden on your retirement income.

The participating whole life insurance path provides flexibility through premium payments tailored to your policy design. It offers guaranteed growth complemented by potential dividends, regardless of market conditions. The cash value remains accessible at any time through policy loans without penalties or restrictions, while providing death benefit protection for your family. Your money grows tax-advantaged, and distributions through policy loans avoid the tax implications of traditional retirement account withdrawals. PWLI also provides a unique ability to use the same dollars multiple times through the policy loan feature, creating a financial efficiency that retirement accounts can’t reach.

Consider how these approaches might play out in real life:

Traditional Retirement Approach: John contributes $8,549 annually to his 401(k). When an unexpected $15,000 home repair arises, he has to either:

Each option either damages his retirement savings or creates high-interest debt.

Participating Whole Life Approach: Sarah contributes the same $8,549 annually to a participating whole life policy. When faced with the same $15,000 expense, she:

Most importantly, once Sarah repays the loan, that money becomes available to her again for future needs. This cycle can repeat throughout her lifetime, creating a personal banking system that keeps her financially stable.

The true benefit of participating whole life insurance isn’t just the death benefit or even the cash value accumulation – it’s the creation of a sustainable financial system that grows over time while remaining accessible throughout your life.

This approach allows you to:

While 401(k)s and IRAs will continue to be part of many Americans’ retirement strategies, the limitations inherent in these accounts make them incomplete solutions for life’s financial journey. Participating whole life insurance offers an approach that addresses the shortcomings of traditional retirement planning while providing benefits that extend beyond retirement age.

The promise of retirement account millionaires is appealing, but the reality often falls short. With only 3.2% of retirees reaching millionaire status through 401(k)s and IRAs – and even those fortunate few potentially outliving their savings – it’s clear that alternative strategies deserve consideration.

Participating whole life insurance is a financial system that provides guarantees, flexibility, and control that traditional retirement accounts cannot. By allowing you to build assets while maintaining liquidity and recovering expenses that would otherwise be permanently lost, it creates a path to sustainable wealth that can last a lifetime and beyond.

For those concerned about outliving their retirement savings or needing financial flexibility throughout life, consider participating whole life insurance.

At McFie Insurance, we specialize in designing participating whole life insurance policies that help people build sustainable wealth to last a lifetime and beyond. We not only design and sell these policies but also guide our clients in how to leverage their cash values effectively for financial stability and security. If you’re interested in learning more about how participating whole life insurance could fit into your financial strategy, we invite you to schedule a consultation with our team.

Tomas P. McFie DC PhD

Tomas P. McFie DC PhD

Tom McFie is the founder of McFie Insurance and co-host of the WealthTalks podcast which helps people keep more of the money they make, so they can have financial peace of mind. He has reviewed 1000s of whole life insurance policies and has practiced the Infinite Banking Concept for nearly 20 years, making him one of the foremost experts on achieving financial peace of mind. His latest book, A Biblical Guide to Personal Finance, can be purchased here.

This free binder has the information to build your own Infinite Banking system.

This free binder has the information to build your own

Infinite Banking system.